China PET bottle chip downstream roundup in Q1 2024

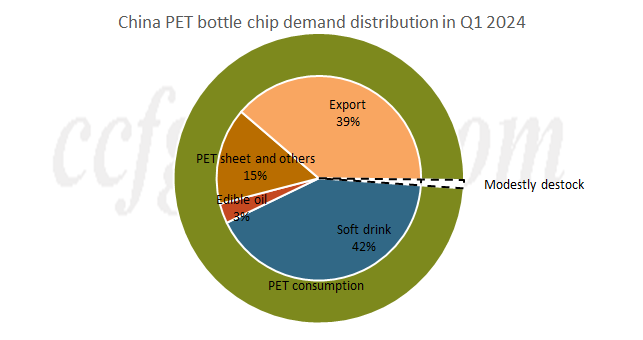

According to the CCFGroup statistics and subsequent data revisions, China domestic demand for PET bottle chip in the first quarter of 2024 is around 2.16 million tons, a 20% increase year-on-year. This growth is attributed to a relatively low base in the same period of 2023 and a significant short-term demand increase due to intensive capacity expansion plans and favorable performance of most beverage companies in 2023. Some large enterprises were reportedly maintaining O/R during the Chinese New Year. Additionally, China's overall price advantage in exports has led to strong replenishment demand in overseas markets, especially with a record high shipment volume in March. The total export volume of PET bottle chip in China in the first quarter of 2024 is estimated to be around 1.4 million tons (combine two HS code volume), showing a 10% year-on-year increase. By the end of March, the total inventory of PET bottle chip in China was around 1.66 million tons, down 40kt compared to the end of the previous year.

In terms of specific sectors, the demand for PET in the bottled water and beverage industry reached around 1.5 million tons in the first quarter, with a 25% year-on-year increase, accounting for approximately 69.4% of domestic demand. The growth is mainly driven by increased production capacity in the beverage sector over the past two years, leading to a significant actual increase in PET demand. Procurement by beverage companies was not much in the first quarter. Post-holiday concentrated replenishment often occurs from late February to March. Due to the satisfactory sales and profit performance of water companies last year, output of mainstream brands still showed significant growth in the first quarter, especially with some company experiencing a short-term surge in demand due to brand PR events.

The edible oil industry also saw a decent increase in PET demand of around 22.3% year-on-year in the first quarter, supported by increased population mobility around the Chinese New Year, contributing to tolerable performance in catering industry, which indirectly boosted demand for PET. However, market was in relative slack season post-holiday, and O/R of edible oil plants maintained at 60-80%, which may gradually rebound to high rates around Dragon Boat Festival holiday (Jun 10)

In the first quarter, demand for PET in PET sheet field showed a poor growth rate, with only a 7.8% year-on-year increase. Currently, the gap between different regions and brands is further widening. The Eastern region, due to the early development of new end-user applications such as fresh produce, milk tea, and coffee, has seen a reasonable increase in packaging demand, with PET sheet plants O/R maintaining at around 60-80% after the holiday. In contrast, the Southern region is facing intensified homogenized competition, with downstream products relatively single, leading most sheet enterprises to opt for recycled bottle flake instead of virgin PET resin to reduce cost losses. However, this strategy has not prevented the region from long-term low operation levels. The Chinese New Year holiday started early, and post-holiday resumption of work was delayed until early March, with operating rate mostly around 40-50% thereafter. Integrated enterprises have relatively higher order volumes, as they acquire obvious cost advantages. O/R recovery is reasonable.

Looking at downstream purchasing trends in the first quarter of 2024, downstream purchases are mainly price-oriented, with many engaging in early restocking around lower price levels. The seasonal impact on purchasing decisions has weakened compared to previous years. The market saw large volume replenishment at prices ranging from 6700-6950yuan/mt in the fourth quarter of 2023 when prices were low. However, as prices rose above 7100yuan/mt, the market's replenishment enthusiasm decreased notably. With expectations of a significant increase in supply due to new capacity expansions, downstream factories and traders are not rushing to make high-priced purchases. Overall, PET resin trading price primarily fluctuated narrowly at 6980-7130yuan/mt.

In summary, China PET bottle chip market in the first quarter of 2024 shows a slight destocking trend, benefiting from a clear increase in domestic demand and the maintenance of export shares. In the second and third quarters of 2024, with more new capacities coming online, which is expected to exceed 4 million tons, potentially intensifying sales pressure both domestically and internationally. By the end of June, factory inventories may accumulate to high levels again, so it is advisable to monitor any changes in plants operation at that time.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price