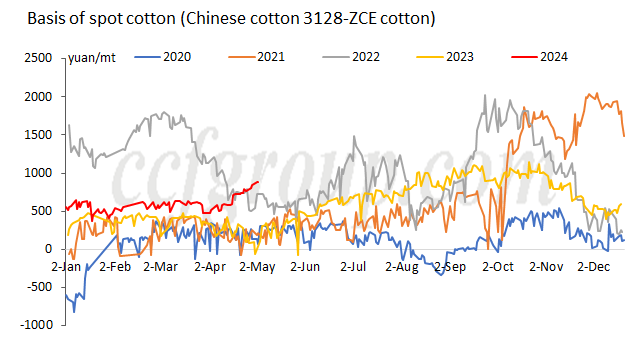

Will continual rise of spot cotton basis support cotton prices up?

From mid-Apr to early May, ZCE cotton futures market has been constantly decreasing, and during the decline, spot cotton sales were active and basis of spot cotton kept upward. Except the high basis in end 2021 and early 2022 caused by the competition for seed cotton procurement, the timing for the basis rising this year is obviously earlier than previous years and the quality cotton gradually tightens. Why does this happen? First, 2023/24 Chinese cotton production is forecast to reduce by nearly 700,000 tons compared to 2022/23 season. Second, as part of large ginners purchase 2023/24 cotton at high costs, it is understood that they are reluctant to sell, with a quantity of nearly 1 million tons. These large ginners have strong financial strength, and are not willing to sell in deficits in short term. Third, though downstream market has no good performance in 2024, the operating rate of spinning mills has not dropped evidently, so the consumption to cotton remains at a relatively high level.

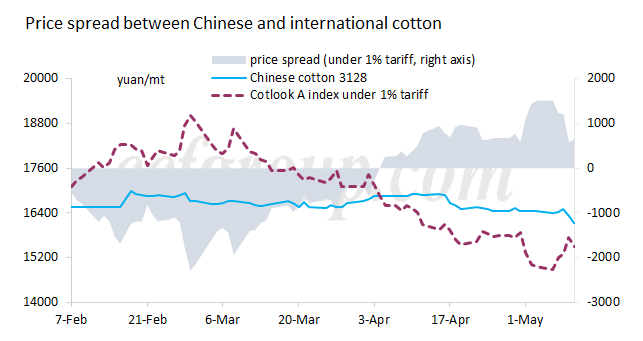

Currently, cotton market has obvious bullish factors, with continual rise of basis of spot cotton and healthy spot cotton inventory. Then will this status help cotton prices go up again? Two supply factors shall be considered: 1. The pressure brought by the continual cotton imports; 2. New cotton production forecast.

Currently, price spread between Chinese and international cotton expands again, and the pressure from cotton imports maintains. Imports are the major supplementary supply, although some imported cotton will be into state warehouses. Till now, there are only 894kt of cotton quotas under 1% tariff in 2024 and the sliding-scale duty quotas that are released in 2023 have been invalid in early 2024. Therefore, whether the imported cotton will has more supply pressure needs to pay attention to the allocation of sliding-scale duty quotas. If the quotas are issued earlier, the pressure from imported cotton will be more obvious.

For new cotton production forecast, new cotton planting condition is good currently, and 2024/25 season is supposed to be a bumper year, putting pressure on the cotton prices later. But it is hard to change the status of gradual tightening spot cotton inventory currently. If large ginners continue to be tight sellers, Chinese cotton supply still faces structural contradiction in short term.

Overall, since mid-Apr, the basis of Chinese spot cotton has increased by over 300yuan/mt. There is a certain structural contradiction, with the gradual shortage of quality cotton. In the short term, this contributes positively to cotton prices. However, attention is needed on whether and when the sliding-scale duty quotas will be issued. If the quotas are issued early, the pressure from imports will remain significant. Conversely, if quotas are issued late, there will still be temporary contradictions in the short term. Additionally, 2024/25 cotton production is expected to be good, which may exert pressure on future cotton prices. Furthermore, macroeconomic still requires attention.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price