PE market in a stalemate

PE market is volatile recently, with a period of continuous rise, and then an endless decline at the end of this month. Downstream buying interest is not high, and most of them purchase to cover their rigid demand. Some are resistant to the current high prices, and some are cautious about the current market and uncertain prospects. The upward trend of LLDPE futures has been hindered to some extent, some of which have been suppressed by the collapse of crude oil and the concentrated outbreak of negative sentiment in the entire international financial market, but it is more dragged down by spot demand. Of course, although spot prices cannot go up, it seems that the downward space is limited, which is mainly supported by the cost side. The prices of crude oil and ethylene are still high and supply is tight. PE, as its downstream products, has been obviously supported.

From the perspective of the market and transactions, when futures prices fall, spot price is still strong, petrochemical plants keep their price firm and downstream buying intention would be promoted; and when futures rise, the rising trend of spot prices is not as obvious as futures, and downstream prefer procure at need-to-basis.

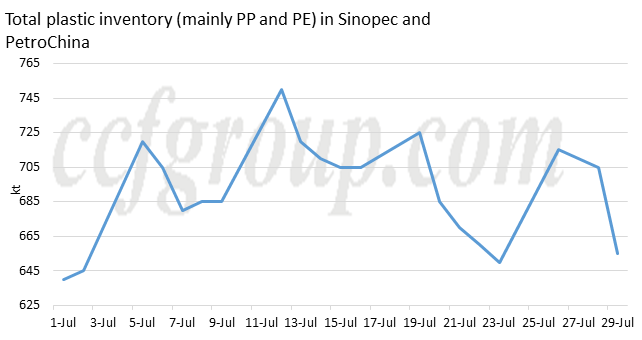

In terms of inventory, the inventory of PetroChina and Sinopec is slightly below the medium level, with an average of about 700kt. At the same time, the inventory of traders, port and downstream is not high. The low inventory level often means that the market still has the potential to rise, but it seems that it is only potential at the moment.

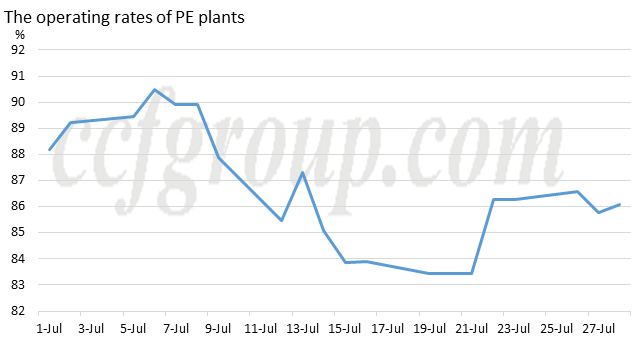

In terms of supply, it is expected that it will be difficult for new capacity to be put into production in August. At present, the operating rate of China domestic PE plants is around 86%. Many plants shut for maintenance for around a month in mid-July. At the same time, there is also some plants plan to shut for turnaround in August, thus the operating rates of China domestic plants may maintain low and domestic supply may be reduced to a certain extent. At the same time, China's PE imports continued to decline in June, reaching the lowest level since February 2018. The reasons are as follows: first, the price spread between China domestic market and the overseas market is large. Second, foreign traders are not unwilling to sell to the Chinese market with low market prices. Also, the sea freight soars, and the containers is in shortage. Therefore, the decline in domestic supply in the short-term is mainly due to the decline in domestic production and imports.

As far as demand is concerned, currently, agricultural mulching film is still in the off-season, and the operating rate and order volume have decreased compared with 2020. Other downstream products is also lukewarm, and purchase the raw material at need-to-basis. On the whole, downstream market steady-to-lower, and it have limit influence in supporting the market.

To sum up, it is not difficult to see that the current PE market is in a situation of low supply and bearish demand, low inventory and poor transaction, in which poor transaction is the main contradiction of lukewarm PE market at present. As long as the spot transaction can be improved, the current stalemate situation is likely to be broken, otherwise it will continue for a period of time.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price