Caprolactam supply still tight in Sep

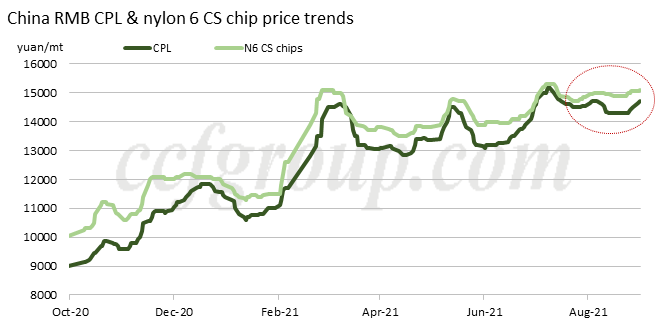

CPL prices have been keep firm through Aug

At the beginning of this month, this website has stated in the insight“Caprolactam price underpinned by low operating rate in short”that the support from tight supply was quite obvious. Since the first week of August, CPL contract was nominated and kept unchanged at 14,700yuan/mt, and settled at 14,600yuan/mt, 6 months payment, ex-works. After that, the weekly guidance price rose to 14,900yuan/mt at the last trading day of the month.

Looking back at the situation in the first half of Aug, it can be seen that both supply and demand have reduced. When upstream crude oil and benzene prices slumped, the price in nylon industrial chain followed down, but the decrease was very limited for CPL and downstream nylon. The factor that has hindered demand in Aug include seasonal effect and expected supply increase in late market.

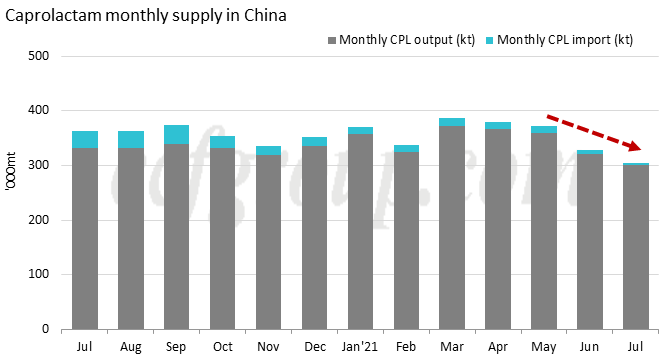

Both CPL production and import drops sharply

CPL production and import volume had kept a declining trend since May 2021, and the sharp decline had been witness in both June and July. Imports of CPL were falling as the price in China became a lowest place in the world when benzene prices hovered high in most areas. Buyers were trying to switch more to China domestic sources.

In Jul 2021, CPL production in Chinese mainland totaled around 301kt, evidently down 19kt from Jun (320kt). China imported 2.84kt caprolactam in July 2021, down 91% from the same period of last year, and down 61% month-on-month. Total CPL supply in July 2021 dropped 16.3% year-on-year, a hardly seen fall in the past few years.

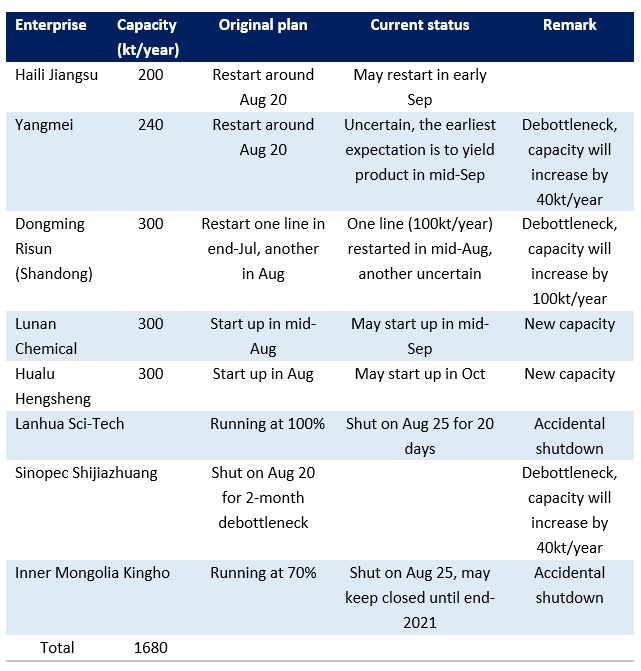

Expectation toward supply increase fails

The saying that CPL supply will increase in Aug has been through the entire second quarter of 2021. Plant restart from turnaround, expansion from debottleneck, and newly added projects had all been planned in Aug, indicating a strong bearish outlook. However, these expectations did not come true until the end of the month, when CPL plant operating rate lingered low at 72%, and no new capacities including any successful debottleneck. Inner Mongolia Kingho, started in July, was the only new supplier in the second half of the year, and it had just meet the urgent need in East China and North China.

Previously expected schedules include Domging Risun (Shandong), Yangmei, and Jiangsu Haili restarted, and there will be a total of 740kt/year of incremental production capacity, and Hualu Hengsheng, Lunan Chemical will bring together another 600kt/year. A total of 1.34 million tons/year of CPL capacity had been expected to put into operation during late Aug until early Sep. However, none of them are fulfilled.

Supply may keep tight until mid-Sep

Based on various sources, CCFGroup currently estimates that CPL supply will keep a tight balance until at least mid-September. According to the latest information, some regions (especially in North China) currently have stricter control of carbon emission, and environmental protections are still strictly monitored, which has caused obvious constraints on the restoration of some CPL producers. In addition, if the restart of Yangmei and Haili is delayed again, with Lanhua and Shijiazhuang Refinery shut for maintenance, the supply in North China and Jiangsu province will be in short again.

Price development in Sep depends on demand

If CPL supply keeps tight until H1 Sep, is it possible for the price to rise further?This question certainly leans on another side, demand. The look in nylon downstream over the past half a month has been mixed.

First, textile industry did not appear good. Nylon filament plants have started sales promotion with lower prices since last week. It is the first time, when upstream CPL and chip prices are steady, while filament plants cut offers to promote sales. And polyester market is also in similar situation as PFY plants are actively restricting production to keep prices. There are rumors about the peak season may not be as good as expected.

Second, the non-textile sectors seem to be better. Modified plastic plants have suffered weak demand since June and their operating rate and feedstock inventory has been cut down. And that is why the low-end sources have been fully digested. Demand for film has been healthy, and its performance in Sep is still under positive outlook.

In conclusion, the recovery of the non-textile sector is relatively certain, as their operation has been more cautious in the past few months, and the product and feedstock inventory status is healthy. The only uncertainty is how much stronger it can be in the coming peak season. However, the nylon filament market, after a bullish performance in H1 2021, has accumulated inventory from fiber to yarn. Facing the uncertainty, they may still cut down operating rate to control risks. And demand for textiles in the peak season still needs to be observed.

All in all, CPL supply is very likely to keep tight in Sep, and downstream players, who have taken a bearish look, are suggested to moderately replenish stocks.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price