PX and PTA profits get squeezed

The decline in China PTA market slowed down in Sep, with prices of spots hovering at around 4,800yuan/mt. However, PTA futures slumped on Sep 8, and spot market moved down in tandem with spot price down to 4,710yuan/mt, hitting new low in two and a half month.

PTA margin was squeezed with price dropping. As of Sep 9, the spread of PTA to PX narrowed to around only 400yuan/mt. Considering the cost of acetic acid, the spread was further lower at around 195yuan/mt.

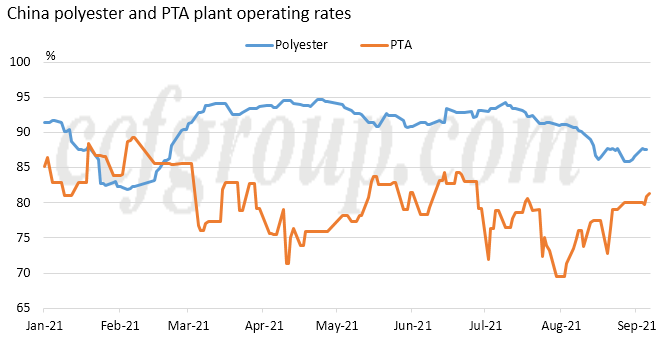

Currently, polyester plant operating rate hovered low and the sales ratio was bleak with participants in the lack of confidence. Scheduled maintenance on PTA plants is limited in Sep, while Yisheng New Materials’fresh 3.6 million mt/yr PTA units have been running stably. PTA inventory is expected to rise by about 300kt in Sep, bringing pressure on PTA market.

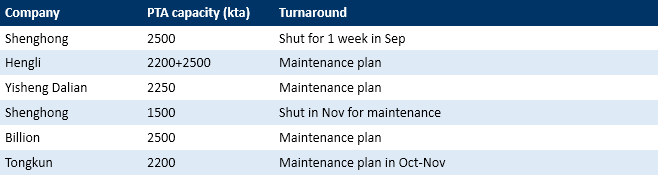

In the medium to longer run, several domestic PTA plants would undergo maintenance.

In addition, with the profits squeezed even to negative territory, some unplanned plant shutdown may take place.

In terms of polyester, the profit has improved, however, it is still under strains from high inventory. Some polyester producers are lowering the prices to boost sales with the nearing of Mid-Autumn Festival holiday in H2 Sep and National Day holiday in the beginning of Oct. Any sharp decline in polyester plant operating rate is unlikely in the short term, while some previously-shut plants may restart with the improvements of the profits of some polyester products.

It is currently estimated that China PTA fundamentals may improve in the fourth quarter, with supply and demand turning balanced or the inventory increasing fractionally. With some plant maintenance expected in Oct-Nov, PTA inventory is anticipated to reduce by more than 100kt during that period.

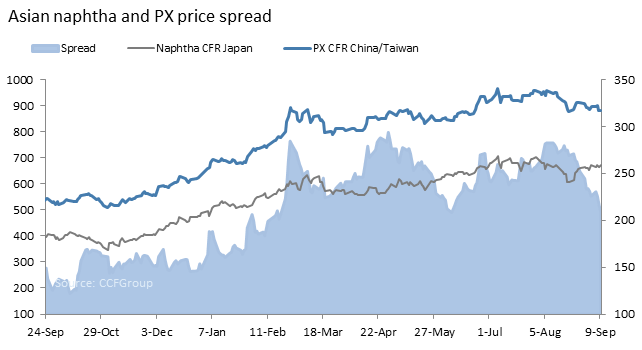

In terms of PX, PX-naphtha spread has narrowed rapidly to $210/mt, as PX is weighed by rising plant operating rate as well as squeeze in PTA margins.

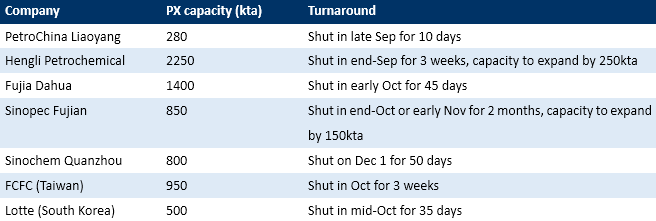

Meanwhile, several PX plants both in China and abroad would undergo maintenance in the fourth quarter.

Therefore, though China PX inventory would pile up in Aug, but may decrease slightly in Sep and could increase only slightly in the fourth quarter, which could be supportive to PX-naphtha spread.

In a conclusion, the profits in polyester and its feedstock chain have been reallocating since July. Polyester sector was under losses earlier, but then the profits of PX and PTA were squeezed due to polyester plant operating rate cuts. Currently, with polyester profits recovering, feedstock PX and PTA are under pressure of losses. With PTA and PX plant maintenance in the future, the supply and demand situation is expected to improve and PTA and PX profits may recover. The recovery may be fueled if upstream crude oil prices drift lower, but it would be difficult for PTA and PX prices to rebound substantially.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price