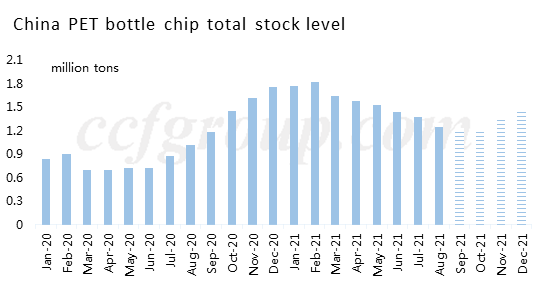

PET bottle chip inventory to pile up with downstream O/R slipping lower

PET bottle chip factory delivery has been a bit tight near end Aug to early Sep, and some time traders and downstream customers said that they need to queue up to pick up the goods, hence PET processing spread once rebounds to 900yuan/mt. However, with weather cooling down in Sep, beverage and water plants operating rate gradually slips down, the delivery tightness is easing. In the fourth quarter, PET bottle chip factory stock and total inventory may both accumulate.

At the end of August and the beginning of September, due to the frequent force majeure of overseas plants, many orders were transferred to Chinese mainland, especially the fourth week of August, when China PET resin export orders exploded. Therefore, PET bottle chip factory delivery both in and abroad were relatively intensive. At the meantime, as a spate of PET resin plants underwent maintenance previously, which is also one of the main reasons to see periodical tightness.

According to CCFGroup statistics, at present, a total of 1.25 million tons PET bottle chip capacity are shut down in overseas market. Due to the serious epidemic situation, most workers are reluctant to go back to work. Billion Vietnam plant shut down near late July, and has not restarted yet. Indorama 550kt/year PET resin line declared force majeure mid-August due to a fire. The unit may turnaround for at least two months. US DAK 450kt/year line also announced force majeure as the local hurricane has affected the supply of raw materials.

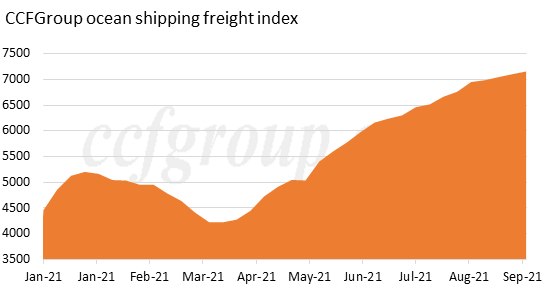

At present, export orders are relatively stable, as there is some demand gap in overseas regions, which could still support PET export prices. Since the third quarter, some overseas customers began to accept bulk form delivery in order to reduce shipping costs. But with demand for bulk goods increasing, freight has also doubled, basically twice the figure of which at the beginning of the year. However, it is still $100-200/mt lower than export freight of whole container delivery. It is known from forwarders that the turning point of ship supply may come after September 2022 (mainly based on the fact that it takes 2-3 years from ship building to formal operation), and unless the epidemic has been greatly improved, the imbalance in the global supply chain may continue to push up freight rates. Players shall prepare to face the challenge of high freight for a long time.

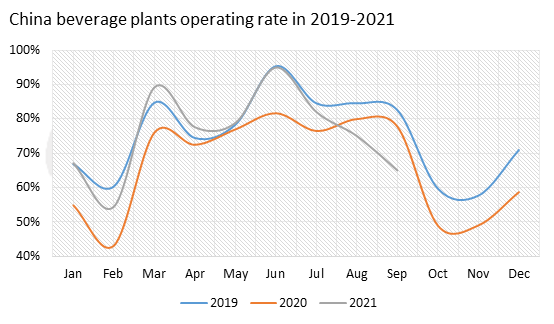

From downstream point of view, the operating rate of large beverage producers basically dropped to 60% in early Sep, with some slightly higher at 70%, while the O/R of some plant in South China remained high. In terms of PET sheet factories, industry run in South China maintains around 40-50%, and East China slightly better at around 70-80%, partly lower at 50-60%. Therefore, near mid-Sep, though downstream pick-up speed slowed down, the market delivery situation has gradually improved.

Note: Sep data is assessed one

Generally speaking, from Sep to Oct, with the recovery of closed plants, market supply will gradually increase, hence PET bottle chip price may face downward pressure and processing spread may shrink. In Q4, there are still some maintenance plans, which is uncertain yet. Export market, overseas plants may not likely to restart within short term, and some may still turnaround in Q4, hence FOB Shanghai price may likely to hover within -20-30 to +20-30 range. There is no big chance to see sharp decline.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price