PE CFR China market keeps firm on account of the high cost and low supply

Since 2021, although the overall trend of PE CFR China market has fluctuated with the RMB market, PE CFR China market price keeps firm. From the perspective of the market outlook, PE CFR China market is still expected to continue to rise, mainly due to the high cost and low supply.

The overseas market price is higher than the RMB market

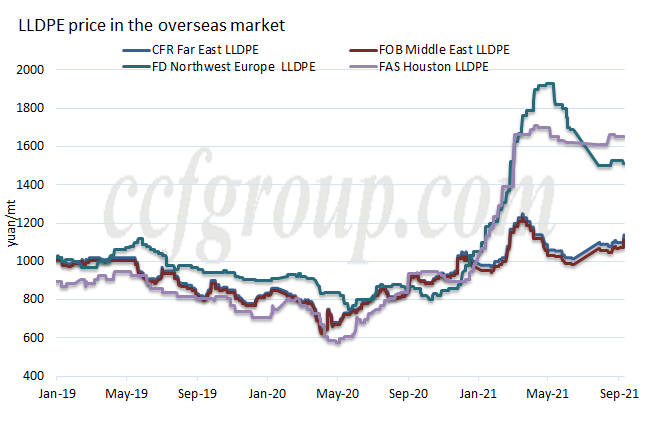

Taking LLDPE as an example, by comparing the prices of the Far East (which can replace Chinese prices), the Middle East, Northwest Europe and Houston, it can be clearly found that the prices in the Far East are much lower than those in Northwest Europe and Houston. It can be said that the prices in overseas regions (especially in Europe and the United States), the price is much higher than those in China, so most of the sources of goods from the Middle East, Southeast Asia and America are given priority to Europe and the United States, and then supply to China would be considered. In addition, more and more new plants in China have started up and the production capacity increased, squeezing out part of the imported goods.

The cost is high, and price spread between RMB market and PE CFR China market is large.

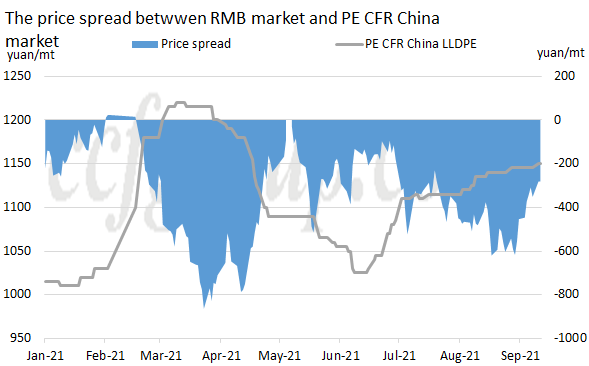

Although the current China domestic prices are lower than those in Europe and the United States, however, for China, suppliers publish their new offers at high price each week, and thus the price spread between RMB market and PE CFR China market was large. Taking LLDPE as an example, as shown in the above chart, LLDPE price in PE CFR China market is continuously higher than that of RMB market, and the price spread is fluctuating around 200-800yuan/mt. Even if the current price spread is around 400yuan/mt, the range has been expanded due to the gradual increase in the price of suppliers’new offers. Under such situation, downstream buyers prefer to purchase yuan-denominated materials and get the tax refunded. Although traders intend to sell USD-denominated materials, market transaction is thin.

The import volume has dropped sharply, and the import supply is tight.

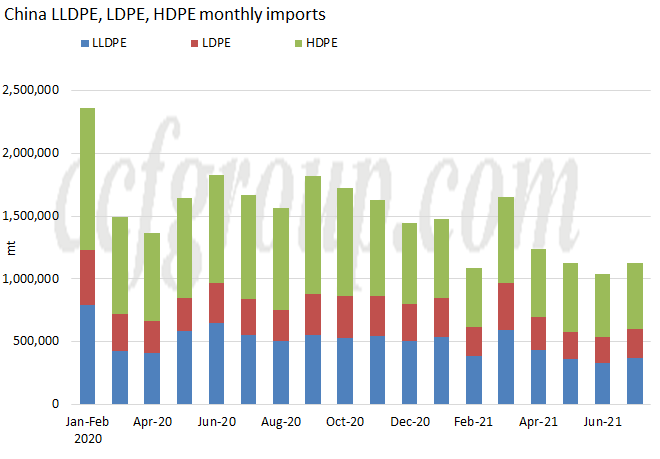

Under the comprehensive effect of the above reasons, China's PE imports have been greatly reduced. According to customs statistics, China's total PE imports from January to July in 2021 are 8.7466 million tons, a decrease of 15.60% compared with the same period in 2020. Among them, LLDPE imports are 3.0152 million tons, down 11.64% year-on-year; LDPE imports are 1.829 million tons, a year-on-year decrease of 1.87%; and HDPE imports are 3.9024 million tons, a year-on-year decrease of 23.30%. It can also be clearly seen from the below chart that the reduction in PE imports is extremely obvious, and there is even a tendency to decrease month by month.

On the whole, with the continuous increase of domestic production capacity in China, there is still an obvious squeeze on the source of imported goods. In addition, the overseas market price continues to be higher than that of China, the suppliers’supply to China has shrunk. For China domestic first-hand traders, high costs (whether raw material costs or sea freight) is always difficult to operate, and the buying interest is weak. Moreover, for downstream, buyers prefer to purchase yuan-denominated materials and get the tax refunded, and buying intention for the USD-denominated materials is bearish. Overall, PE CFR China market will continue to strengthen.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price