Lucrative profit of nylon 6 CS chip sustainable or not

CS chip market turned lucrative in Q4 2021

The first chart is the historical price spread of nylon 6 conventional spinning chips (short as CS chip) chip and CPL since 2016, the trend has continuously spiraled up in the second half of 2021, and reached above 1,400yuan/mt in mid-Dec. And one thing should be noted that the price term of CPL RMB spot is“6 months payment”and that for CS chip is“by cash”, and there should be 100yuan/mt margin added to the actual spread between CS chip and CPL. Therefore, CS chip is 1,500yuan/mt over CPL spot.

And if look as the profit margin of nylon 6 CS chip based on CPL, it had turned from negative zone to a lucrative range in the last quarter of 2021, and peaked at 750yuan/mt on Nov 29, 2021. How did nylon 6 CS chip plants come to the trumps in the last quarter of 2021?

How did CS chip margin improve so much?

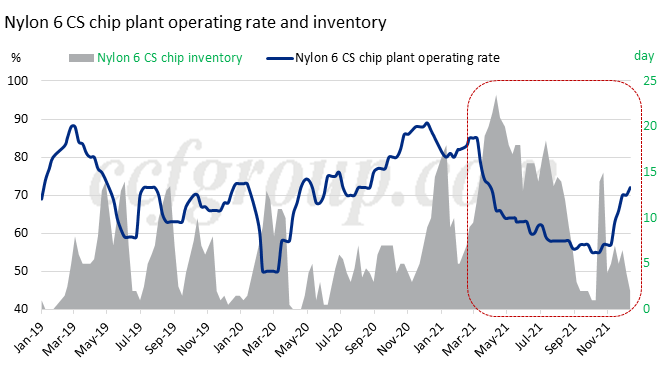

First, it is the long-term low operating rate taken by CS chip plants, which gradually underpins chip prices. Nylon 6 CS chip plants have curtailed production significantly from 85% March, when CS chip plants were suffering losses at the end of the first quarter, to a yearly lowest rate at 55% in late November 2021. The production cut did not help to cease the decline in chip, and inventory has risen to as high as 23.5 days in mid-April and kept high around 15 days by mid-August. It has been a long time struggle for CS chip plants.

Until the latter half of August, CS chip market began to rebound, and downstream came in to replenish intensively and removed the accumulated chip stocks finally. In September-October, CS chip inventory pressure was already low, while as upstream CPL supply remained tight and the dual control policy limited plant operation, the run rate only recovered evidently since November.

Second, the production cut in CS chip gradually burdened down CPL market. Since October, CPL RMB spot has been dropping continuously. Though it is triggered by the slump in coal price, CPL new capacity and limited downstream production and demand also attribute to the price decline. During this period, CS chip plants have gained more power in the price negotiation and they have seized the opportunity to drag down CPL prices.

After CS chip margin reached high level in the beginning of December, most downstream buyers have considered that the lucrative profit in CS chip is not sustainable according to previous experience. However, the firmness in CS chip market is beyond expectation, as when CPL spot dropped to 13,100yuan/mt in early December, CS chip prices rebounded after a short-lived decline to 14,400yuan/mt, to 14,900yuan/mt and higher again. Chip-CPL spread maintains high at 1,350-1,450yuan/mt (actual spread at around 1,500yuan/mt). There comes the final question: is the lucrative profit of CS chip sustainable? When will it fall?

Is the lucrative profit of CS chip sustainable?

Historically speaking, the 1,500yuan/mt price spread between CS chip and CPL is not so out of reason. In the first chart, the core line of the spread was around 1,500yuan/mt in 2017-2018, when the market was relatively bullish.

Here we would like to draw a conclusion of this article first: the lucrative profit of CS chip could sustain for a relatively long period. And below are the three major reasons.

First, the intensive new capacity release is temporarily suspended, and CS chip industry capacity will keep basically steady in a relatively long period. There will only be one 70kt/year nylon 6 chip plant planned in the beginning of 2022, and the rest will be started up since the middle of 2022. In addition, the overall capacity of nylon 6 chip and CPL is likely to be balanced in the year of 2022.

Second, CS chip inventory is low in both chip plants and downstream. Until mid-Dec, downstream plants and traders still hold a small quantity of CS chip stocks, and there is plenty room for them to replenish stocks in late market. The time is uncertain, while buy power is sufficient.

Third, CS chip market is more likely to perform well when HS chip market is weaker. It is an internal balance between HS chip and CS chip market, or CPL contract and spot market. It is because that when high-speed spinning chip market situation is not satisfactory, it will for sure influence CPL contract trading and settlement, and that will give more space for CS chip plants, who could restock both contract and spot CPL. This logic is strengthened when CPL supply is getting looser when more new capacities are released. Actually, nylon 6 HS chip market has evidently cooled down in the second half of the year, and under this circumstance, insiders hold conservative outlook for the market after the 2022 Spring Festival and even the first half of 2022.

Above all, the high profit margin of nylon 6 conventional spinning chip may keep for a longer-than-expected time period.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price