Container marine market: tight shipping space & higher freight before LNY

According to the latest World Container Index assessed by Drewry, the container index rose by 1.1% to $9,408.81 per 40ft container by Jan 6. The average comprehensive index per 40ft container was at $9,409 year to date, around $6,574 higher than the 5-year average $2,835.

After a steady decline in freight for trans-Pacific routes since mid-September 2021, the freight has continued increasing for the fifth consecutive weeks, according to the Drewry index. Freight rates of Shanghai-Los Angeles and Shanghai-New York rose 3% to $10,520 and $13,518 per 40ft container, respectively. The freight is expected to climb up further with the coming of Lunar New Year (LNY for short, Feb 1).

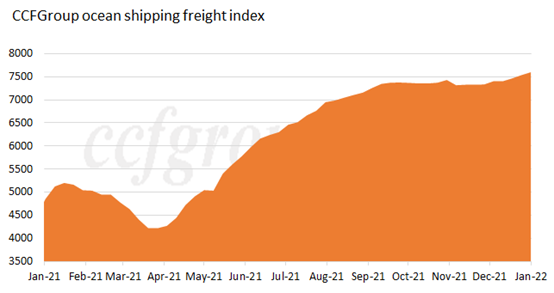

According to the CCFGroup ocean shipping freight index, it has kept rising from Apr 2021 and hit high at the beginning of 2022.

European route:

The spread of pandemic continued in a large scale in Europe with daily new infections keeping refreshing new high. The demand for daily necessities and medical supplies sustained high, stimulating transportation demand to better direction. The pandemic resulted into slower recovery of supply chain. The shipping space kept tight and the sea freight sustained high. The average utilization rate of seats at Shanghai port was high still.

North America route:

The spread of pandemic was deteriorating in US due to the large-scaled spread of Omicron variant and the daily new infections have been 1 million, which exerted negative effect on the recovery of economy. The economic recovery may face pressure in the future. Transportation demand remained high at the beginning of 2022, with stable supply and demand. The average utilization rate of seats in W/C America Service and E/C America Service was still near 100% at Shanghai port.

The average waiting time for container ships in the last week of 2021 was 4.75 days, while the average waiting time for the whole year was 1.6 days in New York port and New Jersey ports.

The shipping capability of container marine market is still constrained. The disruption of inland transport services in US greatly prohibited the shipping capability of supply chain. Meanwhile, the congestion at ports also apparently dragged down the circulation efficiency of shipping capability. According to the data from Marine Exchange of Southern California, as of last Friday, a record 105 container ships were waiting for berths in Los Angeles and long Beach.

As the shortage of equipment at the Asian port of departure continued, the shipping space was also extremely tight. Market demand has been exceeding supply, and prices have been stable at a high level for a long time. Due to the continuous delay and rescheduling of the cargo ships, the reliability of the voyage was very low, and the sailing delay before the Spring Festival will seriously affect the post-holiday shipping. Some carriers slightly raised prices in the first half of January. With the coming of traditional Spring Festival peak season, the price may be really adjusted up in the second half of Jan.

According to the latest data from Drewry, the 3 big shipping alliances in the world will totally cancel 44 sailings in the following 4 weeks, with THE Alliance ranking the first at 20.5 and Ocean Alliance the least at 8.5.

Many shipping companies have released their performance for the first three quarters of 2021 and most saw remarkable achievement:

From Jan to Nov in 2021, Evergreen Shipping's revenue totaled 459.952 billion Taiwan dollars (about 106.384 billion yuan), far exceeding the revenue of the same period in 2020.

In November 2021, Maersk, the world's largest shipping giant, reported third-quarter results with revenue of $16.612 billion, up 68% from a year earlier. Of this total, revenue from the shipping business was $13.093 billion, far exceeding the $7.118 billion in the same period in 2020.

Another shipping giant, France's CMA CGM, reported third-quarter results for 2021, which showed revenue of $15.3 billion and a net profit of $5.635 billion. Of this total, revenue from the shipping sector reached $12.5 billion, an increase of 101% from the same period in 2020.

According to the report for the first three quarters of 2021 released by Cosco, the leading container transportation company in China, the net profit belonging to shareholders of listed companies was 67.59 billion yuan, up 1650.97% from the same period last year. In the third quarter of 2021 alone, the net profit belonging to shareholders of listed companies reached 30.492 billion yuan, up 1019.81% on annual basis.

CIMC, a global container supplier, achieved revenue of 118.242 billion yuan in the first three quarters of 2021, an increase of 85.94% over the same period last year, and a net profit of 8.799 billion yuan belonging to shareholders of listed companies, an increase of 1,161.42% year on year.

All in all, with the approaching of Spring Festival (Feb 1), the logistic demand sustains strong. Congested and disrupted supply chain worldwide and the ongoing spread of pandemic continue arousing large-scaled economic challenges. Some barge service in South China will be suspended with the coming of Lunar New Year holiday (Feb 1-7). The freight demand will sustain strong before holiday and the freight volume will also remain high, while the spread of pandemic is expected to continue affecting the supply chain. That means the new Omicron variant and the Lunar New Year of China will be big challenges for the supply chain worldwide at the beginning of 2022.

As for the forecast for the first quarter of 2022, the freight shipping capability is estimated to be constrained due to the delay of shipment. According to Sea-Intelligence, 2% of shipping capacity was typically delayed before the outbreak of COVID-19 pandemic, but that number soared to 11 % in 2021. The data obtained so far showed that congestion and bottlenecks are worsening in 2022.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price