Nylon 6 uptrend eases with lower risk appetite

Chart 1. China RMB CPL & nylon 6 chip price trends

This round of rising in nylon 6 industrial chain had lasted for a month. Different from previous waves of uptrend in 2021, there were divergences in the process, so the rhythm of increase was relatively slow. In fact, the time given to the downstream for replenishment was also sufficient, but since there was no consensus on the bullishness, the transaction was in a gradual manner instead of explosive rise this time.

Entering the second week in January 2022, the bullish performance has extended after Sinopec raised contract nomination further. However, trading of nylon 6 chip was obviously under pressure, and chip plants have different thought and strategies as well. Some of them insisted on bullish outlook toward the market after 2022 Spring Festival, as supply was still tight. But the others focused on a steady sales and have given some discounts to customers. As the price trend comes to consolidation and slight softness, buy mood is not as high as the previous time.

In terms of supply-demand pattern, both CPL and nylon 6 chip market have kept a healthy balance so far. Since the second half of December 2021, there have been several unstable operations in CPL industry, as some plants have restarted while some had shut or cut production. The result of these issues is almost neutral, and there is no evident skew in the supply-demand balance.

Figure 1. CPL plant operations in Dec 2021-Jan 2022

| Company | Capacity (kt/year) | Operation status |

| Luxi Chemical | 200 | Shut on Dec 3 and restarted on Jan 5 |

| Yangmei | 100 | Restarted in early Dec, but ran at low rate |

| Hualu Hengsheng | 300 | Run rate lowered to 40-60% with upstream since Dec 6 for two weeks |

| Hubei Sanning | 140 | Shut on Dec 13 for 3 days |

| Sinopec Baling Petrochemical | 270 | Third line restarted on Dec 24, recovered to 100% by end-Dec |

| Luxi Chemical | 100 | Shut on Dec 30, restarted on Jan 3 |

| Yangmei | 100 | Accidentally shut in early Jan, the other 200kt/yr line ran at low capacity |

| Sinopec Baling Petrochemical | 270 | Overall O/R lowered to 40% since Jan 6 for 10 days |

| Haili Jiangsu | 100 | Restarted on Jan 6 |

| Luxi Chemical | 100 | 100kt/yr line recovered to normal operation by Jan 7, 200kt/yr line may restart on Jan 10 |

| Shenma | 300 | Operation unstable since end-Jan, production waved largely |

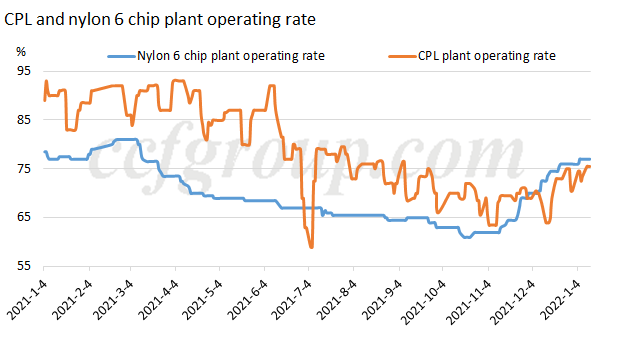

Chart 2. CPL and nylon 6 chip plant operating rate

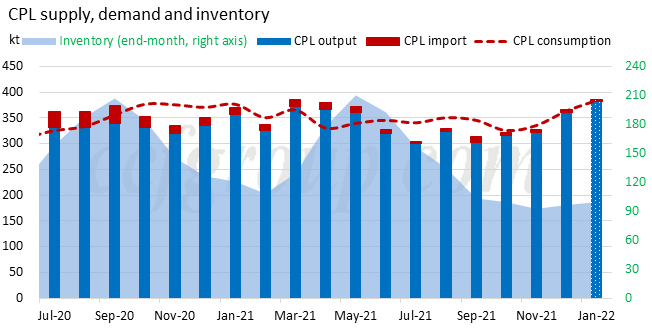

The above chart shows that the core lines of the average operating rate of CPL and nylon 6 chip plants basically keep a same pace. And in the below chart we could see that CPL inventory has been relatively stable over the past two weeks.

Chart 3. CPL supply, demand and inventory

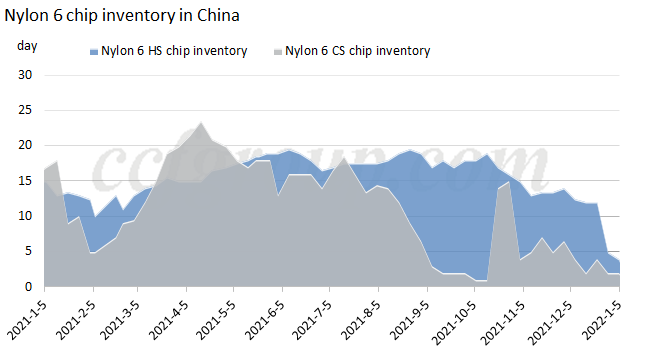

In terms of nylon 6 chip inventory, CS chip inventory has slightly increased this week, while there is no pressure on CS chip plants yet. Nylon 6 HS chip prices maintain firm, mainly due to reducing supply from low-end sources. It is quiet certain that the January contract settlement will be rising month-on-month, therefore, downstream buyers have actively restocked for HS chip, and consumed up the stocks rapidly. Both nylon 6 CS chip and HS chip inventory are low.

Chart 4. Nylon 6 chip inventory in China

Despite of a healthy performance on market fundamentals and continued firm trend of upstream benzene cost, the mentality of nylon players have changed. After the price rise for about one month, there is narrower power upward. In addition, downstream markets are entering holiday mode, and logistics will be soon ended. Transactions of all industrials have reduced.

The most important thing is that market insiders are still not certain about the post-holiday market, and it is difficult to judge whether it will rise or fall. Therefore, the operation tends to be conservative, and the risk control is the main strategy.

Taking chip plant as an example, the current CPL spot price is not appealing to chip plants. CPL spot price has reached 14,300yuan/mt, and the Jan contract settlement is mostly expected at around 14,500yuan/mt. The spot price is considered a relatively high rate in comparison with the contract price (contract CPL market is considered to be high-end sources, and the prices are normally higher than the spot.) As a result, chip plants mostly have no intention to restock CPL spot now. At the same time, chip suppliers are negotiating the February orders with downstream buyers, and forward sales for Feb will be slightly lower than the spot rate. However, according to market feedback, the trading is not satisfactory.

The current pricing is still favorable for chip makers. In a conservative forecast in Feb, an active sales strategy is reasonable. The buy mood is also influenced by the expectation that Luxi Chemical will restart its CPL and polymer production in the second half of Jan, which will certainly cause pressure to both CPL and nylon 6 chip spot, and there may be further price adjustments in chip market.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price