Interpretation of USDA's Sep supply and demand report on cotton

Recently, USDA has released Sep supply and demand report, which maintains a neutral to bullish outlook. For the monthly change, 2022/23 global cotton beginning stocks and ending stocks are forecast lower, while production and consumption are forecast higher. For 2023/24 season, beginning stocks, production, imports, consumption and exports are forecast lower, as well as ending stocks, which is bullish somewhat.

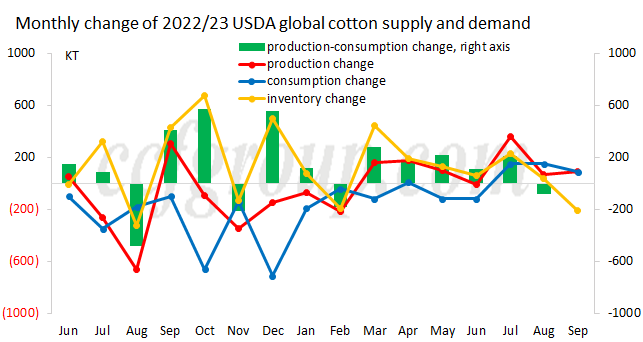

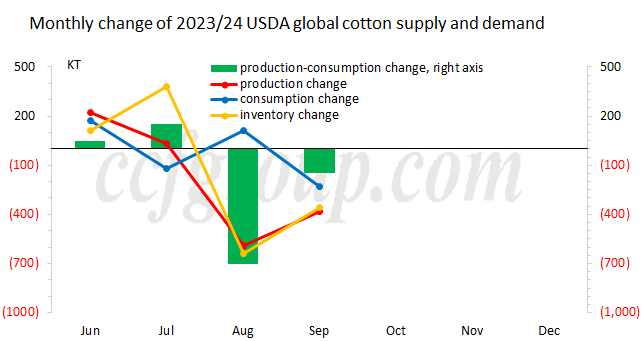

1. USDA Sep supply and demand report

In the USDA Sep report, the adjustments for the 2022/23 global cotton supply and demand were relatively small. The main changes were a reduction in beginning and ending stocks, with China and Turkey seeing a decrease of 110,000 tons and 190,000 tons in beginning stocks respectively. Correspondingly, the ending stocks were also adjusted downwards. Global cotton production was slightly increased, mainly contributed by Brazil with an additional 110,000 tons. The consumption was mainly adjusted upwards for China, adding 110,000 tons. With the decrease in beginning stocks, China's ending stocks reduced by 210,000 tons. As a result, the global ending stocks decreased by 210,000 tons to 20.29 million tons.

As for the monthly adjustments in the global cotton supply and demand for the 2023/24 season, there were several notable changes. The global cotton production was further reduced by 380,000 tons, with the United States decreasing by 120,000 tons and India decreasing by 110,000 tons. However, Brazil increased its production by 110,000 tons. Global cotton imports were slightly reduced by 130,000 tons, with Vietnam's cotton imports lowered by 70,000 tons. The global consumption and export volumes were both adjusted downward by 230,000 tons and 130,000 tons respectively. India, Bangladesh, and Vietnam saw reductions in consumption, while the decrease in export volume mainly came from India. The cumulative adjustments to global ending stocks were lowered by 360,000 tons. With a reduction of 210,000 tons in beginning stocks, the net decrease in ending stocks amounted to 150,000 tons.

2. U.S. cotton good-to-excellent ratio reaches a multi-year low, and worries over the production remain

Before the release of the USDA's adjustment to the US cotton production, there were various speculations in the market. Many believed that the significant downward revision in Aug had gone too far and expected a slight rebound or correction in Sep. However, considering the recent weather conditions and crop growth in the main cotton-producing regions of the US, it is not surprising to see a downward adjustment in production. Although there has been increased rainfall due to recent hurricanes, soil moisture conditions remain severe. Currently, the drought index has reached 185, which is 60 points higher compared to the same period last year. The drought index in Texas, in particular, has reached 306. Moreover, the good-to-excellent ratio of U.S. cotton crops also reaches a multi-year low. By the week ending Sep 17, good-to-excellent ratio of U.S. cotton crops was at 29%, 4% lower than the same period of last year.

3. Brazilian cotton inventory pressure emerges and exports speed up

Thanks to favorable weather conditions, Brazilian cotton is expected to be a bumper year. The USDA has once again increased its estimate for the 2022/23 Brazilian cotton production by 110,000 tons. However, as planting was delayed last year, the harvest progress has been slower this year. Additionally, the exports have been delayed due to tight availability of shipping space caused by a large number of agricultural products being shipped together, leading to increased accumulation in warehouses and putting pressure on domestic storage capacity. As a result, the basis for cotton has been continuously weakening. With the arrival of new cotton on the market, domestic export sales in Brazil have picked up. As of the second week of Sep, cumulative cotton exports reached 63,500 tons, with a daily average export volume of 12,700 tons, an increase of 44.25% compared to the same period last year. It is expected that the export volume will increase by 120,000 tons in the new marketing year, which is reasonable.

4. The shortfall of rainfall in India expands, and production and consumption is expected to be lower

As of Sep 8, 2023, the total planting area for cotton in India reached 12.4995 million hectares, which was slightly lower than the same period of the previous season by 18,800 hectares, representing a decrease of 1.5%. As the rainfall deficit continues to widen, the expectation of a bumper harvest has gradually shifted to a reduction in production. Additionally, the effectiveness of new cotton varieties in controlling cotton bollworm has weakened, which has increased concerns about the production. While there has been some improvement in rainfall in certain regions of India recently, the two major cotton-producing states, Gujarat and Maharashtra, still face historically low levels of rainfall, significantly impacting the overall production. Furthermore, this year, the downstream textile sector in India has been sluggish, leading to reduced demand for cotton, and the adjustment of ending stocks has yet to be made in light of the decrease in production and consumption.

5. Conclusion

USDA makes downward revisions in global production and consumption in its Sep report. Adverse weather conditions have caused a shift from abundant to reduced production in the northern hemisphere, raising concerns about supply tightness. As global consumption has yet to recover and expectations for a weak peak season are strong amid high cotton prices, downstream orders have remained weak and the disconnect between upstream and downstream has not been reversed. Although the production cuts provide some support to cotton prices based on the adjustment of the USDA balance sheet, the lack of improvement in consumption makes it difficult for cotton prices to continue rising. In the short term, ICE cotton futures may be in weak adjustment.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price