Imported PE market review in H2 2023

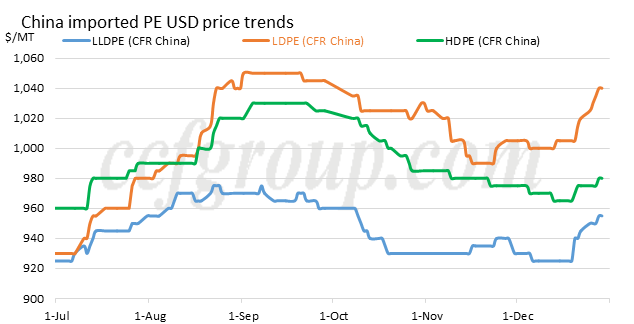

In the second half of 2023, the market exhibited a complex and fluctuating trend, which rushed up first and then fell down, followed by a volatile upward movement.

In July, LLDPE futures surged, providing significantly support to the imported PE market. However, the RMB against USD exchange rate continued to depreciate, and high-price offers were limited. In the middle of the month, RMB market continued to move up, and RMB appreciated. The price spread between RMB market and CFR China market narrowed, and traders offered higher slightly to balance the price spread. Downstream inquiry atmosphere was active. Then, the market softened, and the price could be discussed lower. The market warmed up again due to rising costs at the end of the month.

In August, suppliers raised up their prices, and RMB market strengthened. Most traders offered higher, and market trading was active. However, the depreciation of RMB during this period to some extent restrained excessively high offers in US dollars. Some traders tested the market with lower price, but the support from the stronger RMB market remained, and mainstream offers stable-to-higher.

In September, the depreciation of RMB in the early period remained the dominant influencing factor in the market. Although the RMB market was still strong, transactions for high-price materials were not smooth, and low-priced offers gradually increased. Downstream purchased on need, but speculative demand noticeably declined. Then, the market was mixed, but the overall price moved down. Downstream purchased on need, and towards the end of the month, there was a considerable increase in transactions due to some pre-holiday replenishment needs, mainly at lower prices.

In October, trading was subdued during the National Day holiday. However, there was a significant drop in overnight crude oil during the holiday, and after the holiday, RMB futures-spot market declined. New offers from suppliers declined, and traders successively lowered their offers, and downstream demand was limited. Then, due to the strong LLDPE futures and a rebound in overnight crude oil prices, some offers rebounded. However, transactions for high-price goods was bearish, and traders purchased on need.

In November, market prices remained stable, and in some cases, prices even slightly dropped due to the decline in the RMB futures-spot market and weaker overnight crude oil prices. Market sentiment was relatively low. In late Nov, with the continuous appreciation of the RMB, traders were not willing to sell at low price, and there were even some minor rebounds in certain grades. Downstream demand was moderate, and traders purchased on need.

In December, due to the weak RMB market, some traders offered lower. However, RMB futures-spot market rebounded and RMB temporarily appreciated, and market price of each grades inched up, with some grades showing noticeable price increases. Downstream demand improved.

From the perspective of market characteristics, imported PE market in the second half of the year has the two main characteristics:

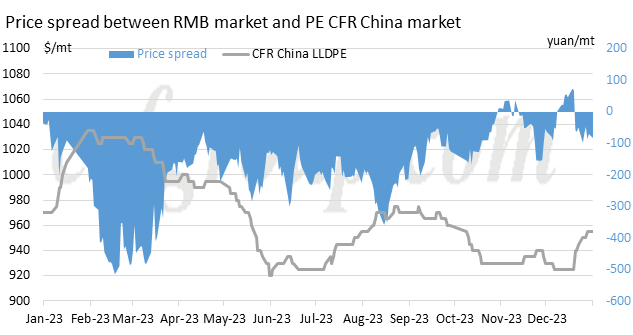

1. The price spread between RMB market and imported PE market narrowed gradually.

In the second half of 2023, imported PE prices still experienced fluctuations. Traders adjusted their offers based on the exchange rate and the RMB spot market, which led to a significantly narrowing of the price spread. In the later part of the fourth quarter, there was even a short period where RMB price was higher than that of imported PE market.

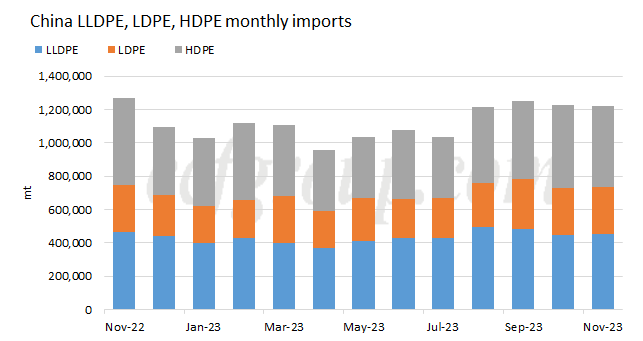

2. Import volume increased significantly.

The total import volume of PE from July to November was around 5.948 million tons, a year-on-year increase of about 2%., which already approached the total import volume of 6.324 million tons in the first half of the year. With the inclusion of December's data, it is expected that the import volume in the second half of the year will increase by about 10-15% compared to the first half. Since August, the monthly import volume has consistently been above 1.2 million tons, mainly due to the market upward trend and the strong demand in the third and early fourth quarters, which has provided certain support to the market.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Futures

- Polyester Price

- PTA Price

- cotton yarn price