Optimistic in polyester filament yarn market despite short-term selling pressure

Impacted by the production suspension on downstream market due to the Spring Festival holiday, the inventory of POY was at 22.7 days and that of FDY was at 19 days by Feb 20. The comprehensive weighted inventory of POY/FDY was at 21.6 days (based on 0.7 of POY inventory+0.3 of FDY inventory).

Current PFY inventory of downstream plants is above 20 days. If downstream plants resume normal production from Lantern Festival (Feb 24), current PFY stocks can guarantee production until mid-Mar. That means polyester companies are likely to face some selling pressure before end-Feb. Sales ratio of PFY was near 30% recently. The inventory of PFY is expected to rise further later and may be high in end-Feb, estimated to be around 26-27 days, higher than the same period of 2023. Downstream buyers may intensively purchase in end-Feb/early-Mar, which should be noted.

PFY market is anticipated to face some selling and inventory burden in short run. However, in long run, sales of PFY may increase and the stocks are likely to reduce based on the following two reasons:

Firstly, the net increase of PFY capacity will be the least in 2024, estimated to be 1160kt/year (500kt/year of capacity will be launched in end-2024). 950kt/year of capacity will be phased out (750kt/year of unit from Yijing is expected to suspend production for one year due to the relocation and Lianda's 200kt/year unit is eliminated due to the resettling). That means the net increase of PFY capacity is estimated to be 210kt/year, with growth rate at 0.4%. Meanwhile, downstream fabric and DTY market is expected to see around 4% of growth.

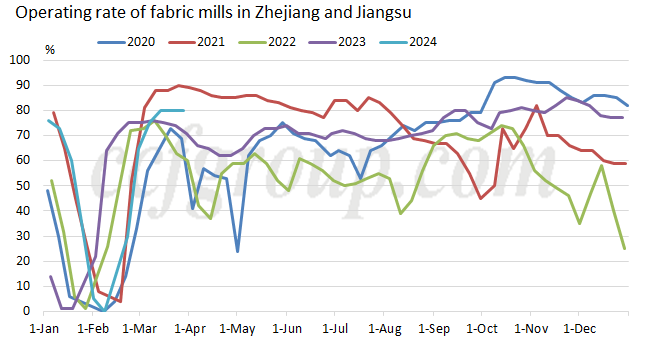

Secondly, most downstream plants, including DTY plants, fabric mills and printing and dyeing plants, will resume operation from Feb 17 to Feb 25 after the Spring Festival holiday, while their operating rate will become normal after Feb 24 as it will take time to see all non-local workers return to work. The operating rate of fabric mills is expected to rise to 60-70% in end-Feb. After market recovers further in early-Mar, the operating rate of downstream plants is estimated to ascend further. The operating rate of fabric mills may be as high as 80% near mid-Mar. Optimistic view is held toward the operating rate on downstream market in Mar-Apr. The operating rate of fabric mills in Zhejiang and Jiangsu in Mar and Apr may be higher than the same period of 2023.

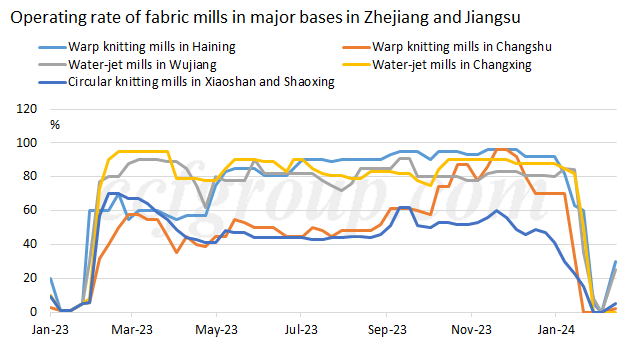

The major reasons are as following: operating rate of water-jet fabric mills was apparently higher than that of knitting mills after the Spring Festival in 2023, with the run rate of warp knitting hitting multi-year low. Some traders had many stocks of knitted winter fabrics affected by the COVID-19 pandemic in Q4 2022 and most were inactive in restocking for domestic sales in the first half of 2023. In Q4 2023, domestic demand was sound and sales of winter goods were smooth. The stocks of knitted fabrics reduced better than other links, which lays a solid foundation for high operating rate in the first half of 2024.

All in all, when the net increase of PFY capacity is very small in 2024 and downstream plants are expected to run higher capacity in Mar-Apr compared with the same period of last year, destocking may be a trend on PFY market although it faces selling and inventory burden in short run after the Spring Festival holiday. PFY market is anticipated to be under destocking track in Mar. The profit of PFY market also deserves anticipation in Mar and Apr. Actual downstream orders should be highly concerned later.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price