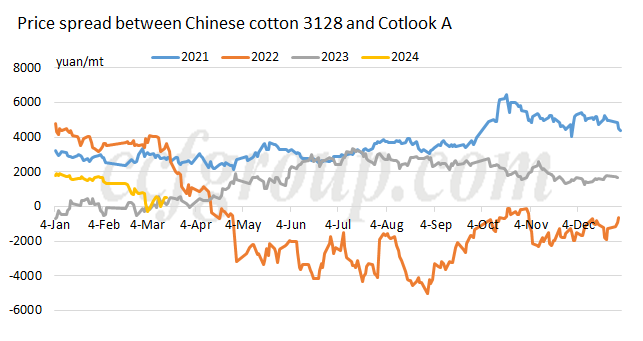

Price spread of Chinese and foreign cotton keeps narrowing, how is the outlook?

Since the beginning of 2024, the price difference between Chinese and foreign cotton has continued to shrink, as shown in the graph below. The price difference has decreased from around 2000yuan/mt in early Jan to near 0yuan/mt (Note: the graph shows the price difference between Chinese cotton 3128 and RMB price of COTLOOK A Index). The market is paying close attention to why the price difference has been continuously shrinking since the beginning of the year and the future market expectations. In light of this, we would like to briefly discuss some of their own views on the matter.

1. Why has the price difference been continuously shrinking since the beginning of the year?

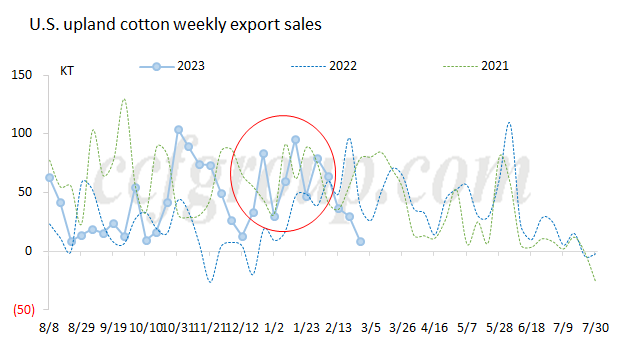

Since the beginning of 2024, ICE cotton futures market maintained a strong trend, while Chinese cotton performance has been relatively weak, mainly due to the stronger demand in the foreign market compared to the Chinese market. From late December 2023 to the end of January 2024, the weekly U.S. cotton export sales have been performing well, especially with good demand from China, quickly pushing the progress of export sales from around 70% to around 90%. At the same time, there were fewer delivery receipts for ICE cotton, and the strong demand performance set a good basis for the upcoming near-month delivery of ICE cotton. However, the marginal improvement in Chinese demand before the Spring Festival was mainly from early December 2023 to mid-January 2024. After mid-January, there was no further marginal improvement. Instead, the market found insufficient confidence due to poor new orders after the Spring Festival. Therefore, when the foreign market was strong, the Chinese market was relatively weaker, leading to the continuous contraction of the price difference between Chinese and foreign cotton.

2. What are the future market expectations?

In the short term, excluding the impact of capital sentiment, the fundamental situation still maintains a pattern of strong foreign and weak Chinese trends. With the foreign market remaining relatively resilient with export sales progress above 90%, as long as there is no significant sales reduction and good export shipment progress later on, while in the Chinese cotton sector, downstream new orders have not improved so far, yarn inventory continues to accumulate, and the pressure on the demand side is gradually increasing. However, attention needs to be paid to whether there will be significant repurchases in U.S. cotton later on and whether the expectation of lower U.S. cotton sowing areas in March will have a negative impact. If the ICE cotton declines and Chinese demand does not improve, the support for Chinese cotton will be weaker.

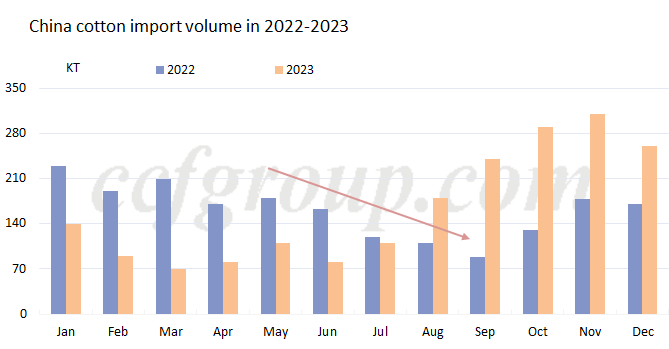

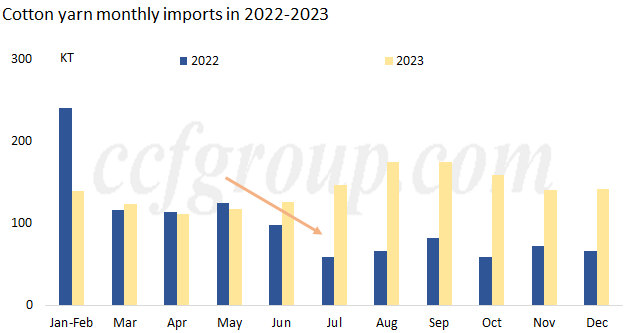

Looking at the medium to long term, apart from the expectation of higher U.S. cotton production and the possibility of the recovery of price difference between Chinese and foreign cotton, the lower Chinese cotton prices than foreign cotton has affected the imports of cotton and yarn, gradually reducing the Chinese supply in the long term. However, the impact of imports on supply will not be reflected quickly and will need time to adjust. Drawing a comparison with the more pronounced situation in 2022, where the Chinese cotton prices began to be higher than foreign cotton in March 2022, but the reduction in imports of cotton and yarn started to gradually show from June. Looking at the situation in 2024, the quantity of cotton imports in China from January to April may still be relatively large, which means that the supply will remain sufficient in the short term, and the decrease in the import volume of yarn may be earlier than that of cotton. Therefore, the impact of imports on supply is more likely to be seen after May or June.

Overall, in the short term, the pattern of strong foreign demand for cotton compared to Chinese domestic demand remains unchanged. However, in the future, attention should be paid to factors such as the U.S. new cotton production condition, the impact of the price difference between Chinese and foreign cotton on the imports of cotton and yarn, and the differences in Chinese and foreign demand. The impact of the imports of cotton and yarn on supply will still need time to manifest.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price