The rise in processing fees for nylon 6 CS chip

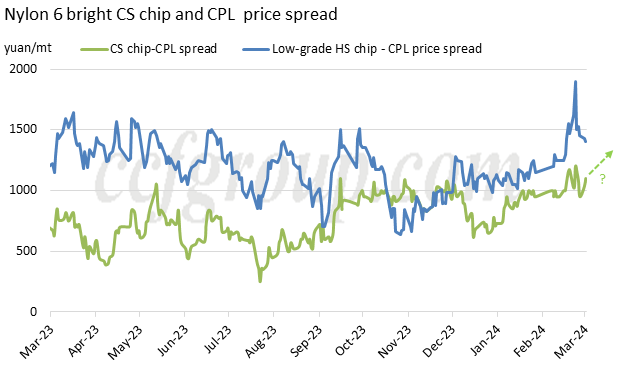

Before and after the Chinese Lunar New Year holiday, there have been significant fluctuations in raw material prices, but the processing fees for nylon 6 chips have remained at a relatively good level. In fact, apart from the spike in processing fees for nylon 6 bright conventional spinning (CS) chip have been mainly steady and healthy, except for the period in the latter half of December and the beginning of January, when CPL prices surged. Looking at the trend in below chart, there seems to be a sign of further strengthening in the near future.

The good processing fees can be attributed to three aspects:

1. The sharp drop in CPL prices in the short term, especially last week's inventory crisis triggering CPL dumping sales, in contrast to a slower decline in chip prices, leading to passively expanding processing fees.

2. The supportive factors of the repair in processing fees for bright CS chip in the fourth quarter of 2023 continued into the first quarter of 2024. The production switch from bright CS chip to semi-dull HS chip occurred in September and October last year, improving the supply-demand pattern in bright CS chip. Since then, there has been no significant increase in supply (only about 70,000 tons from Qizheng), while demand has been relatively strong in modified plastic industry in the fourth quarter of 2023 and first quarter of 2024. Although film market weakened from the fourth quarter to the first quarter, its capacity increased, and the operating rate was relatively high, so the overall supply-demand pattern of CS chip was still good.

3. It was due to the high inventory costs. Before the Chinese Lunar New Year holiday, the mainstream market sentiment was bullish, and the sharp drop in CPL prices this round caused the previous period's inventory, whether CPL or chip finished products, to have relatively high costs. Although CPL prices have dropped to around 13,000yuan/mt, the high inventory costs mean that factories will choose to maintain high processing fees and turnover for a period of time to reduce their previous inventory costs, which is quite common.

For positions trapped before and after the Chinese Lunar New Year holiday, we evaluate them based on a CPL price of 14,000yuan/mt. With the current drop to 13,000yuan/mt, the average CPL cost may still be around 13,500yuan/mt. Bright CS chip prices in East China are currently around 14,200-14,300yuan/mt, and the "actual" processing fee is estimated to be around 800yuan/mt, barely maintaining cash flow. Of course, the actual implementation by factories may vary slightly, but the general situation is as described.

From the supply side, there will not be much capacity released before the end of April, and demand will not yet enter the off-season, so the processing fee will not systematically weaken. However, from a short-term cost perspective, CPL price is difficult to push up due to ample supply, so the 13,000yuan/mt price level may continue for a period of time. As chip factory's raw material cost gradually decreases, the current processing fee of around 1,200yuan/mt or even higher may contract.

Of course, there are two exceptions. One is if polymer market is generally bullish again, leading to sellers' general reluctance to sell at low prices and stubbornly holding onto processing fees. The other situation is if CPL experiences a new round of sharp declines, it may give rise to another round of a passive expansion of processing fees for CS chip. However, from the current factors, the probability of these two scenarios is low.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price