Lower-than-expected nylon filament demand in Aug

NFY transaction in Aug hit year-to-date lowest

August used to be the transitional month from traditional slack to peak season. Actually, downstream has already begun to warm up early in Aug. However, the resurgence of COVID-19 cases in Nanjing, Yangzhou, Zhangjiajie and Zhengzhou, etc., and outside China, had put downstream interest down. Facing the uncertain consumption and high cost pressure of the other raw material spandex, weaving and spinning mills held strong risk-prevent attitude, and focused on digesting previous stocks and only restock at need-to basis. Under this circumstance, purchasing volume of nylon 6 textile filament had evidently dropped.

Reasons for the apparently declining procurement of NYF

1. Poor order taking in weaving and knitting mills

For weaving and spinning mills, the primary reason for reducing purchases and output in August was that their orders did not gradually increase as they did in the same period in previous years. And in the off-season from June to July, the weaving and spinning mills were producing at a significantly higher rate than the same period in previous years. This was mainly due to the strong growth in end user’s exports in the first half of the year, which injected the market confidence toward the peak season in the second half of the year.

▲Resurgence of COVID-19 cases affects downstream demand

However, the resurgence of pandemic cases around several regions in China had hit the market with a cold snap. Although it had little direct impact on nylon industry, market’s expectations toward China domestic demand in the peak season weakened. Downstream stocking tended to be cautious instead.

In addition, the number of new cases surged international in August, which caused further worry about the delivery of end user’s product and the impact on demand. Therefore, it hindered the negotiation of export orders during the peak season. The pandemic has hindered the negotiation of mid and downstream orders in August, which has increased negative expectations of China domestic and export demand.

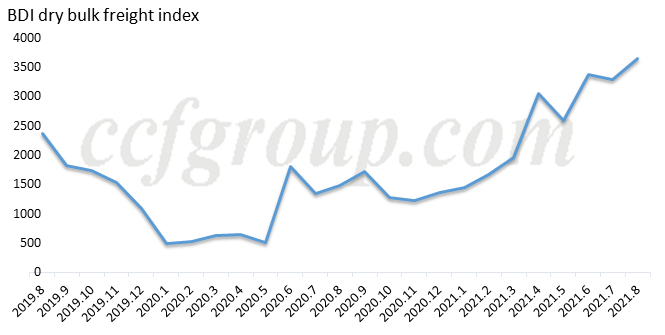

▲Pressure of rising freight rate

Another major factor damaged export orders is the rising freight rate. Due to quarantine requirements, the shipping cycle has been lengthened, and insufficient port staff has prolonged the delivery time. And the lack of labor force caused the shortage of shipping vessels as well. Combined with multiple reasons, increased comprehensive costs since the outbreak of the pandemic in 2020, freight rate has soared and hit a new high in August. According to feedback from some clothing companies, freight rate this year has increased by 5-6 times compared to that before the pandemic. The cost pressure of and the uncertain factors of shipping time have severely hindered the negotiation of export orders.

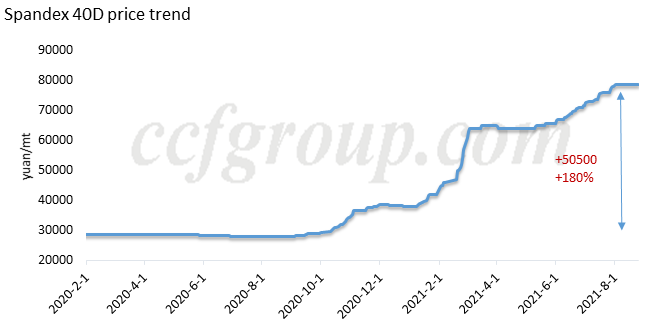

2. Influence of spandex price surge

Another factor affecting downstream mentality is the surging price of spandex. Spandex has continued rising since the fourth quarter of 2020, spandex 40D has risen by 180% compared to the lowest rate in 2020, and the growth of some sources is even more.

As the "accessories" in the production, the cost of spandex has risen above that of the "main materials". Recently, some traders had yielded in prices to promote sales, while some spandex plants were still raising offers. But for downstream buyers, they already began to worry about future downward risks, and they had already took a cautious mode of purchasing, and has lowered the operating rate moderately. They are controlling the risks by the strategy of“order first and then replenish feedstock”. As the main material, purchasing of nylon has also been affected.

In addition, the price of nylon is also at a relatively high level during the year. Sinopec has settled the Aug contract for CPL at 14,600yuan/mt, which is just below the settlement in July. The price remains high in slack season, and this is hard to active downstream replenishment. Though nylon filament plants have been yielding in prices by 300-500yuan/mt since mid-Aug, and some even yielded more than 1,000-1,500yuan/mt, downstream weaving and spinning mills are still purchasing moderately and have low intention to build stocks. It is expected that in the short run, nylon filament market may still be dominated by rigid-demand discussions, and the real peak season will truly usher when there is substantial improvement in end user’s order taking.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price