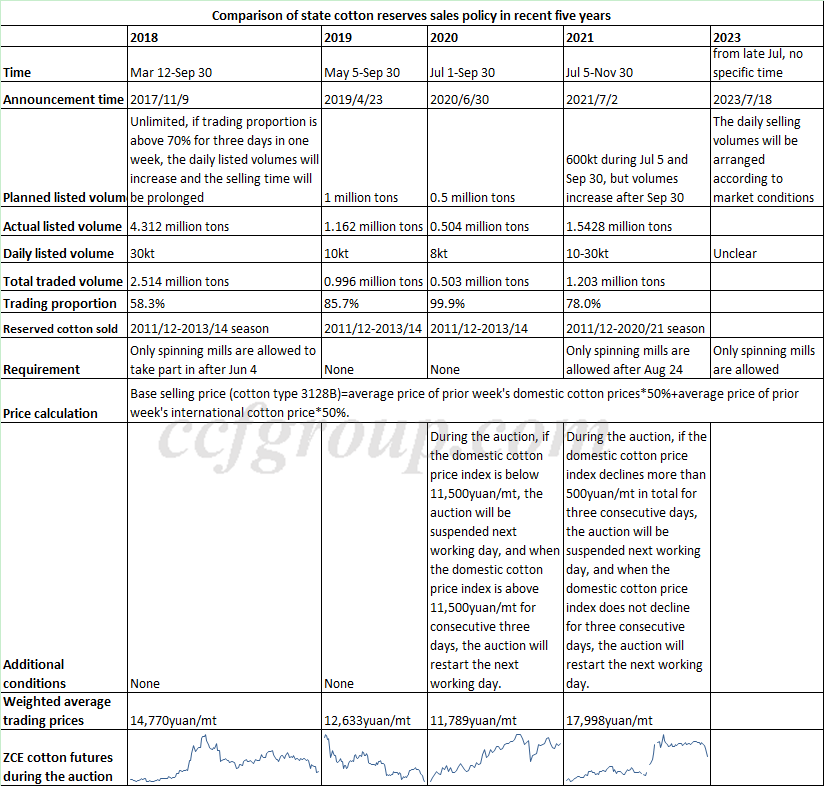

Changes and interpretation of 2023 China state cotton reserves sales

2023 China state cotton reserves sales policy was announced on the night of Jul 18, 2023. What surprised everyone the most this time was no specific selling volumes of reserved cotton, which differed from the market's previous speculation of a fixed amount. This led to various speculations in the market. Some market participants believed that the absence of a specific volume indicated a "sufficient supply" and had a slightly bearish view, while some market participants thought that the state cotton reserve was employing a "bluffing strategy" and had a slightly bullish view. As a result, ZCE major cotton contract declined by about 300yuan/mt during the night trading session on Jul 18. And the further details on the reserves sales policy are awaited. Before the specific details are released, let's analyze from the 2023 cotton reserve sales announcement and the transaction situation of the reserves sales in 2021.

Looking from the announcement, the selling volumes of reserved cotton were confirmed in 2019-2021, even there was no specific volume in 2018, the announcement also stated clearly that the total volumes were unlimited and the daily selling volumes would increase if the trading proportion was over 70% for three days within one week. But in 2023, there is no specific total selling volume and the daily selling volume will be arranged according to market conditions. The rumors about the total selling volumes were 300kt from mid-Jun and there was expectation that the policy would be released on Jun 30, leading to ZCE cotton futures market rise over 400yuan/mt. But after the government announced officially and there was no specific selling volumes, the government does not want the fixed quantity of the reserve sales to cause significant fluctuations in cotton prices.

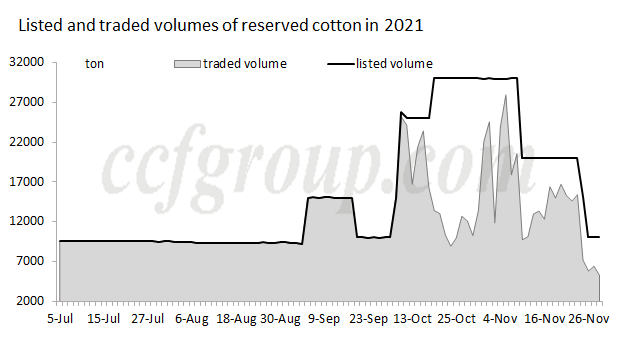

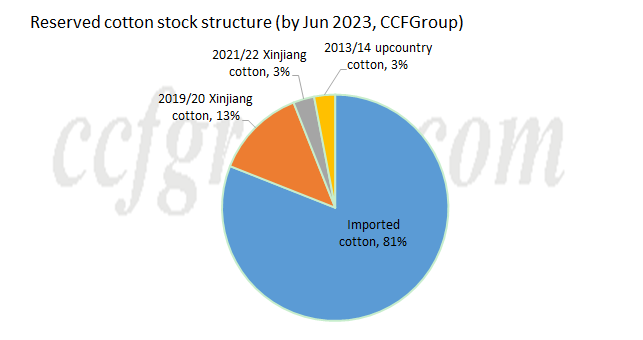

For the total selling volumes of reserved cotton, initially, the volumes in 2021 was 600,000 tons, but as the cotton price rose, additional quantities were released. In the end, a total of 1.54 million tons were listed for sales, and the actual transaction volumes were 1.2 million tons. The daily selling volumes gradually increased from about 10,000 tons to around 20,000-30,000 tons. The reserve sales finally ceased on Nov30, 2021, when ZCE cotton futures experienced a sharp decline. Therefore, it can be observed that the higher the cotton price rises, the more incentive there is for the National Cotton Reserves to increase the selling volumes. This is considered from both the perspective of maximizing profits for the reserves and ensuring supply and stabilizing prices. Therefore, there is no "bluffing strategy" involved. Moreover, market estimates suggest that the inventory of the reserved cotton is at least around 3 million tons, indicating that the National Cotton Reserves still have the capacity to release a similar quantity as in 2021.

In terms of the selling price, according to the Chinese and international cotton prices during Jul 10 and Jul 14, if the cotton reserves sales kick off during Jul 17 and Jul 21, the base selling price will be around 16,737yuan/mt for grade-3128. As the state reserved cotton are mainly the imported cotton from 2018/19 to 2022/23 seasons, the quality discounts may be limited, so the final trading prices may be at least 17,000yuan/mt (the detailed price shall be observed according to the actual transaction condition later). But final trading prices may be slightly lower than the trading prices of spot cotton in inland warehouses. Currently, the spot cotton, 28mm and 28gpt, is pegged at 18,000yuan/mt and above in inland warehouse. Therefore, if the daily selling volumes are large, the reserves sales can ease the cotton supply, weighing on the market in medium to long run. If the auction is fierce, the price of reserved cotton may be gradually higher in short.

Remark: as the reserving volumes of imported cotton are not public, the stock proportion may has certain deviation.

In 2021, the daily selling volumes of reserved cotton were initially around 10,000 tons, and prices were 2,000-3,000yuan/mt higher than the base selling price, leading to gradual rise of prices. Later, as ZCE cotton futures surged over 20,000yuan/mt and daily selling volumes increased to 20,000-30,000 tons, the price increase slowed down, and trading proportion reduced. Therefore, if the daily selling volumes are not large first, the supply effect brought by reserved cotton may be appeared in the later stage.

For the influence of state cotton reserves sales on ZCE cotton futures, according to the ZCE cotton futures trend in the table above, in the medium stage, the state reserves sales could not change the obvious supply and demand contradiction. In 2021, ZCE cotton surged over 20,000yuan/mt under the procurement competition among the ginning factories and price spread between Chinese and international cotton also expanded apparently. Therefore, if there is a large reduction in 2023/24 Xinjiang cotton production and obvious procurement competition for seed cotton among ginners, it may not change the trend of cotton prices being more prone to rise than fall in the mid-term. However, in the long run, it can create supply pressure.

Therefore, in medium run, it is important to pay attention to the supply-side contradictions resulting from factors such as weather conditions, production and seed cotton procurement in Xinjiang, as well as the strength of contradictions between reserve sales and demand. If the supply-side contradictions are significant, cotton prices are likely to continue to rise with difficulty in falling. Meanwhile, the calculation of base selling price of reserved cotton sales is bearish somewhat to the price spread between Chinese and international cotton. Chinese cotton prices will be paid more attention to monitor the foreign cotton prices. Currently, hot temperature prevails in Texas, the United States. If the weather condition is unfavorable, ICE cotton may drive up ZCE cotton, while if the weather condition improves, the ICE cotton may exert downward pressure on ZCE cotton.

In short run, keep an eye on the daily selling volumes of reserved cotton and the trading prices. In long run, the government does not wish for a sharp rise in cotton prices that could harm the industry. Therefore, it is also necessary to monitor whether sliding-scale duty quotas are issued and whether there are other policy guidelines in place.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price