China PET bottle chip market outlook not as bad as expected after cutting down massive output ?

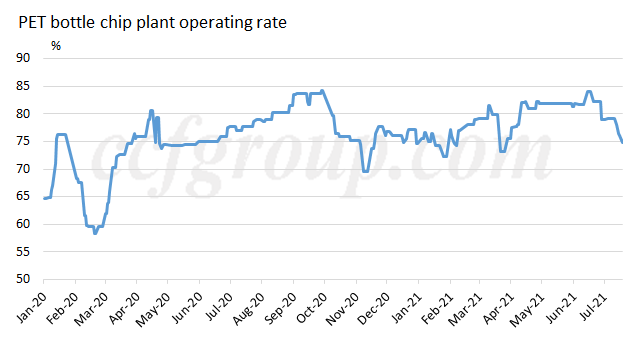

Recently, PET bottle chip factories begin to announce output cut plans, and operating rate of many plants has declined. So far, output of China Resources, Wankai, Indorama Guangdong, Dragon Special Resin, Sinopec and Baosheng has declined in varying degrees, involving a total capacity of about 1.64 million tons (excluding long-term shut Chengxing line). If add the 1.2 million tons long term shut line, the total capacity involved reaches 2.84 million tons. Average operating rate of China PET bottle chip plants has dropped to slightly below 75%. (82.8% based on designed capacity of 12.46 million tons)

In fact, this round of intensive output cutback and shutdown comes from two factors: first, the processing range of PET bottle chips has been compressed within 600yuan/mt for a long time, resulting in reduced profit space; second, new order intake both in and abroad are not good. The continuously rising sea freight due to tight supply of containers and delay of shipping dates makes it even more difficult for PET bottle chip factories.

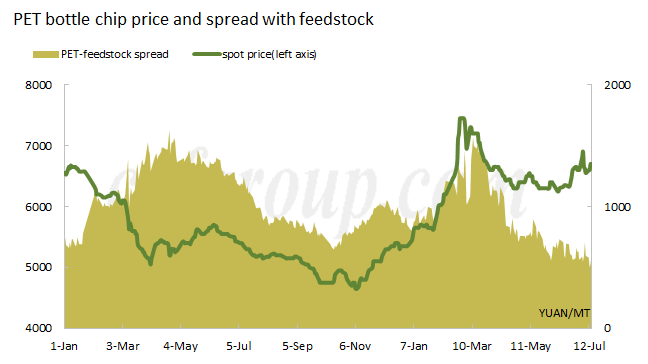

First of all, the compression of the processing spread is caused by two sides, factories promotion and the rising raw materials cost. On the one hand, PET bottle chip industry is now highly concentrated, capacity of TOP4 PET bottle chip factories occupies more than 70% of the total. If one of the factories reduces production, the market share is bound to be divided by other factories. Recently, selling price of one large PET bottle chip manufacturer is relatively low, as its processing spread is basically reduced to around 500yuan/mt. This way, many other bottle chip factories with poor cost advantage are difficult to get new order. The reduction in cash flow forces some factories to consider cutting down output or simply stopping for a period of time. On the other hand, the recent rise of polyester raw materials is relatively fast, even if there is correction, the polymerization cost is as high as 6100yuan/mt plus. Till last Friday, spot polymerization cost stands at 6159yuan/mt, and Jul average level is near 6103yuan/mt. As of Jul 16, PET bottle chip traded price is less than 6700yuan/mt, thus processing spread is lower than 600yuan/mt calculated on average feedstock cost, which means loss for most bottle chip producers.

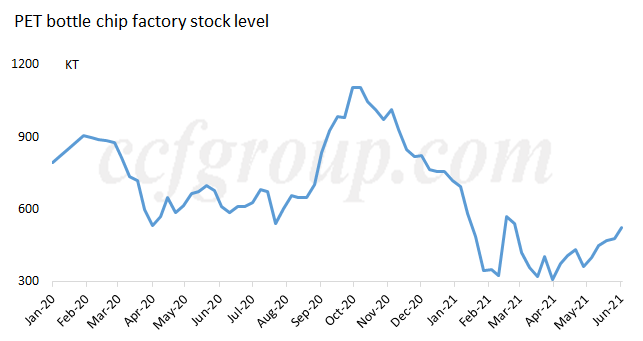

Second, poor new orders are a clichéthis year. In terms of domestic sales, speculative hoarded stock has been high in China, and even though the market digested hundreds of thousands of tons this year, current figure is still relatively high. According to rough statistics, PET bottle chip inventory is around 1.5 million tons, including 500kt (36%) in bottle chip factory, 500-600kt (34%) in the intermediate circulation link and end-user plants, and 400-500kt (30%) speculative hoarding materials by players outside the industry. So far as we know, many speculative hoarding goods have been more than half a year, whose packaging and quality cannot compete with the newly produced products, so the price will be lower than the prevailing market price. Some goods are even untaxed, hence there are not many that really break into the mainstream consumer market. However, there are many traders in the market, the grapevine generally spreads widely, and the mentality of small and medium-sized traders is usually fragile because of their low cash flow. Once there is low-price news, it is bound to drag down the market transaction price.

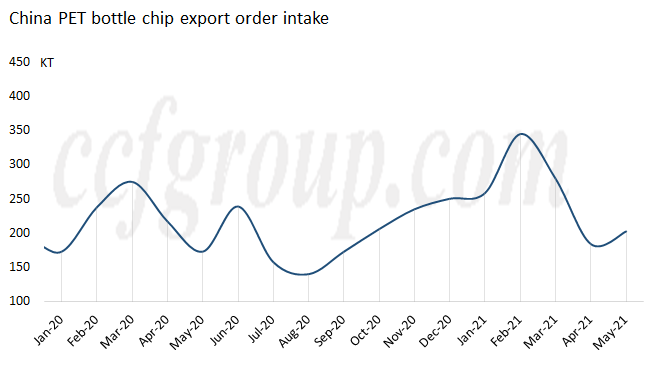

In terms of export, in fact, PET bottle factory order intake is relatively stable, but the constantly hiking sea freight has indeed brought a lot of pressure to the negotiation of new orders. Coupled with the delay in shipping date, we can often see the gap between order intake and delivered goods when looking at the figures issued by the customs. In other words, when we see poor monthly order intake, the shipping volume is not necessarily small. PET bottle factories are not willing to pay more demurrage charges, hence they generally try to make one-time delivery as much as possible.

From CCFGroup point of view, PET resin exports in the second half of the year may not be pessimistic. First of all, the spread of the Delta mutant virus has led to a resurgence of cases in overseas areas. The epidemic has rebounded in many countries and regions in Europe and the United States, and the demand for epidemic prevention and daily necessities has increased. In the short term, the relationship between supply and demand is still tense. Under the background of serious port congestion around the world, the demand of China's export container transport market remains high. So even if the sea freight continues to rise, Europe and the United States still have to import from China and other parts of Asia, especially under the expectation of the peak demand season for Christmas and New Year holidays. We believe that the future global demand is still in a growing trend. The increase in sea freight rates is likely to continue until early 2022.

However, at home, there is still a certain amount of over-the-counter low-priced hoarding stocks, and it will keep depressing domestic sales in the future. Therefore, the industry may need to wait for the listing of futures. Formal trading models and platforms will gradually replace the trading situation that relies solely on market news. By then, the influence of over-the-counter goods is not expected to be as great as it is now.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price