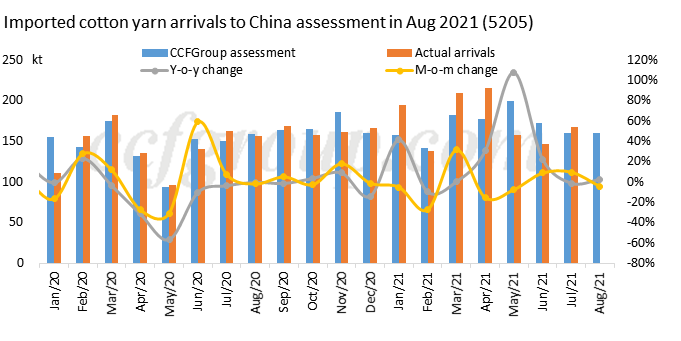

Aug’21 cotton yarn imports may move down 4.3% m-o-m to 160kt

1. Imported cotton yarn arrivals to China assessment

Cotton yarn imports of China in Jul reached 168kt, up 3% on the year and 14.3% on the month. It amounted to 1,231kt cumulatively in Jan-Jul, up 24.9% year on year, and up 3.3% from the same period of 2019. The imports in Aug is initially assessed at 160kt, down 4.3% on the month.

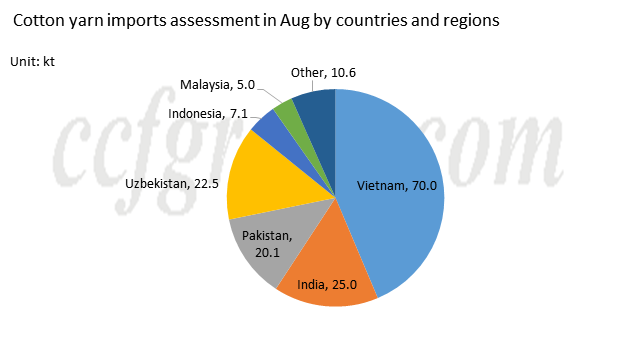

According to export data of foreign markets in Jul, cotton yarn exports of Vietnam did not reduce much, just a small decrease, but the pandemic in Vietnam forced the mills in some regions to reduce production, and the ports were closed and shipments were delayed. Some Jul shipments were postponed to Aug. Therefore, cotton yarn imports of China from Vietnam in Aug is estimated less. Cotton yarn exports of Pakistan in Jul slumped as favorable local demand reduced the products available to be exported, and high price of cotton and cotton yarn prevented China’s buying. In Aug, it may slide compared with Jul. Aug arrivals from India and Uzbekistan is expected to inch up on the month as Indian cotton yarn and Uzbekistan one showed advantages against later shipments and higher price of Vietnamese cotton yarn. It is initially estimated that cotton yarn imports of China in Aug from Vietnam is at 70kt; from Pakistan 20kt, from India 25kt, from Uzbekistan 23kt and from other regions 23kt.

2. Imported yarn stocks declined

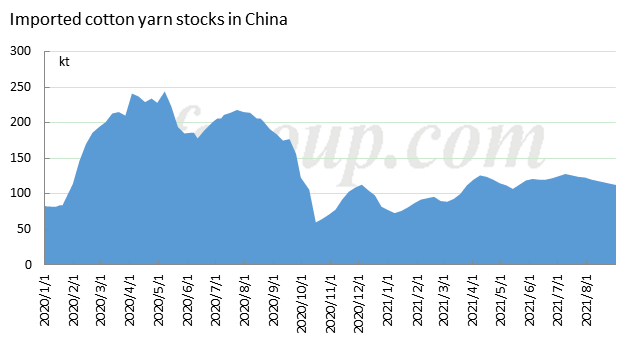

Arrivals of cotton yarn imports of China in Aug declined, and the sales were slow, so the stocks did not reduce quickly in fact. In early and mid-Aug, the price of imported cotton yarn moved up first and then stabilized, but weakened gradually in late Aug. The tight supply of some varieties were eased, but structural issues still existed. At present, siro-spun cotton yarn supply was adequate, as well as 26S and 20S, while C21S and OEC21S were tight. Traders sold mostly with thin profit and large fall of price occasional happened.

Aug was a transit from dull season to peak season traditionally. However, cotton yarn market performed well in Jun and Jul but weakened in Aug. It was mainly due to the macro factors and advanced downstream orders. Overall cotton yarn orders softened in Aug and market confidence was pressed. The operating rate of weavers plunged, both in Guangdong and Nantong, Jiangsu. The impacts were mainly from macro environment, downstream demand, pandemic and power restriction.

In terms of later market, the pandemic in Vietnam remained severe in Aug. The soaring sea freight rate and unexpected improvement of downstream orders in China burdened cotton yarn market. Cotton yarn price moved down and more trades were done with thin profit. The spot stocks of imported cotton yarn was at a medium level and the high price of forward price lent some support to spot one. However, if downstream demand keeps poor and traders of Chinese cotton yarn undersell, spot imported cotton yarn will be under pressure. Looking from previous ordering, the arrivals of Sep will be mainly ordered in Jul when the pandemic in Vietnam was serious and a large amount of production was cut in the South. Therefore, Sep arrivals of Vietnamese cotton yarn is likely to drop, those of Indian and Pakistani one will be limited and those of Uzbekistan will be a bit better. On the whole, Sep arrivals of cotton yarn imports will keep around medium level or less.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price