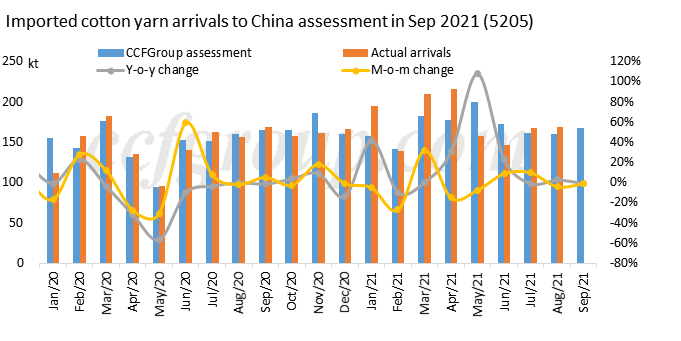

Sep’21 cotton yarn imports may move down 1% m-o-m to 167kt

1. Imported cotton yarn arrivals to China assessment

Cotton yarn imports of China in Aug reached 168.9kt, up 7.9% on the year and up 0.8% on the month. It amounted to about 1,400kt cumulatively in Jan-Aug, up 22.6% year on year, and up 3.6% from the same period of 2019. The imports in Sep is initially assessed at 167kt, down about 1% on the year and month.

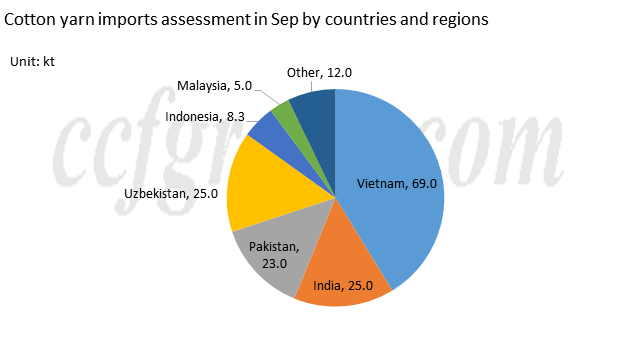

According to export data of foreign markets in Aug, cotton yarn exports of Vietnam saw a small decrease on the month partly because the pandemic delayed the export. The control and prevention measures in southern zone surrounding Ho Chi Minh have been eased, but the spinners still ran at low rate amid severe pandemic. On the other hand, orders of mills in central and southern zones performed well. Therefore, overall exports to China did not slump and remained relatively stable. In Sep, this situation may sustain. Cotton yarn exports of Pakistan in Aug increased. They were ordered in Jul when the buying sentiment of siro-spun yarn in China was mild. Sep arrivals to China are expected to increase further. Aug arrivals from India and Uzbekistan have not been released, but looking from yarn and apparel exports, India’s Aug exports is assessed to decline slightly on the month and Uzbekistan’s may remain stably upward. It is initially estimated that cotton yarn imports of China in Sep from Vietnam is at 69kt; from Pakistan 23kt, from India 25kt, from Uzbekistan 25kt and from other regions 25kt.

2. Imported yarn stocks at average level

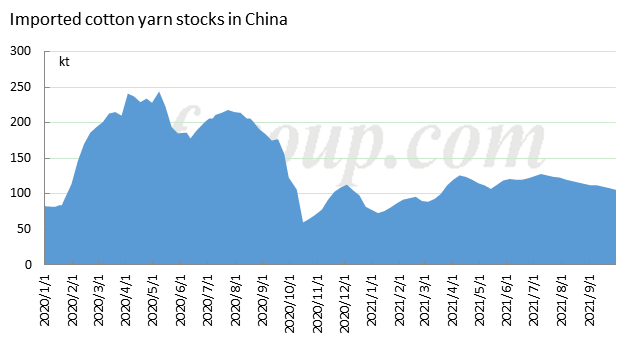

Arrivals of cotton yarn imports of China in Sep declined, and the sales were reported to be slow. The traditional peak season did not show bullish sentiment it should have been. On the contrary, downstream operating rate slid sharply weighed by dual control on energy consumption and electricity restriction. Cotton yarn was sold slowly and traders lowered prices with upset mindset. However, looking from the inventory, structural issues were relieved.

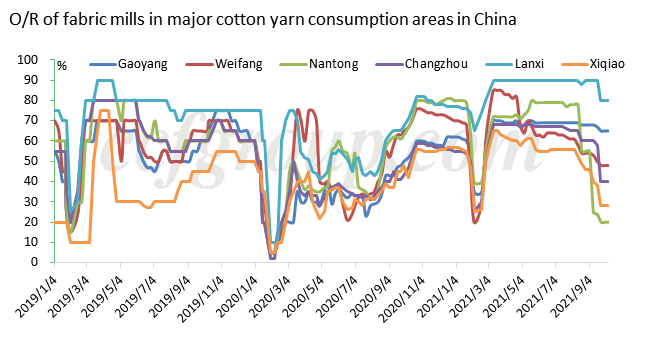

Under the dual control, many regions including Nantong of Jiangsu, Shandong, Shaoxing of Zhejiang and Foshan of Guangdong introduced measures to limit the power use successively in Sep, which directly influenced the operating rate of textile and apparel enterprises. In general, the impacts on downstream weavers were more than that on spinners, with overall operating rate of weavers down to about 40%, including Nantong 20% and less than 30% in Foshan. The enterprises in Lanxi where the operating rate was relatively high also suffered power limit in turn.

In terms of later market, the pandemic in Vietnam remained severe in Sep with low vaccination rate, and the operating rate has not recovered. In addition, Indian and Pakistani local markets did not see good sales. The prices of forward and spot imported cotton yarn both declined and the trading volume was less than expected. Oct arrivals are mostly cargos ordered in Aug. In terms of the orders, those of Vietnamese cotton yarn were mainly placed to central and northern mills which have limited capacity; those of Indian cotton yarn were not many and the prices had large negotiation room; those of Pakistani cotton yarn were relatively less; those of Uzbekistani cotton yarn were relatively stable. Therefore, looking from Aug orders of traders, Oct arrivals will remain above-average.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price