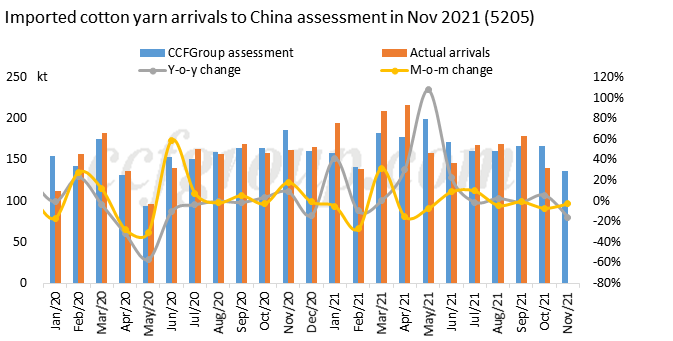

Nov'21 cotton yarn imports may move down 2.8% m-o-m to 136kt

1. Imported cotton yarn arrivals to China assessment

Cotton yarn imports of China in Oct reached 140kt, down 11.1% on the year and 21.8% on the month. It amounted to about 1,719 kt cumulatively in Jan-Oct, up 17.1% year on year, and up 2.5% from the same period of 2019. Affected by forward imported cotton yarn higher than spot one for long term, the ordering volume of China reduced gradually. The imports in Nov is initially assessed at 136kt, down about 26.7% on the year and 2.8% on the month.

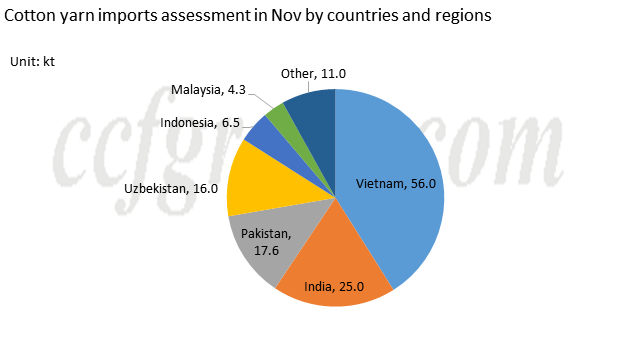

According to export data of foreign markets in Oct, cotton yarn exports of Vietnam continued to decrease on the month. During the second half of Oct to the first half of Nov, Vietnam’s cotton yarn exports reduced about 17%, so the part to China will also decline. Cotton yarn exports of Pakistan in Oct increased by 10% on the month, and that to China may also move up. India’s cotton yarn exports in Oct also showed downtrend. Nov arrivals were mostly ordered in Sep and the first half of Oct. At that time, orders were placed intensively as ordering opportunity appeared, but they may arrive in Nov and Dec. Therefore, Nov Indian cotton yarn arrivals are estimated to reduce. Uzbekistani cotton yarn was partly shifted to other countries without price advantage to China, so Uzbekistani cotton yarn arrivals are expected to keep below 20kt. It is initially estimated that cotton yarn imports of China in Nov from Vietnam is at 56kt; from Pakistan 18kt, from India 25kt, from Uzbekistan 16kt and from other regions 22kt.

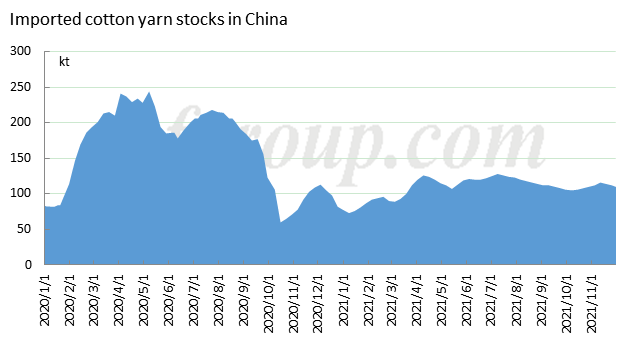

2. Imported yarn stocks show downtrend.

In Nov, spot imported cotton yarn was sold slowly with price dropping continually, but due to the small amount of arrivals, the actual stocks reduced slightly. Overall supply was adequate.

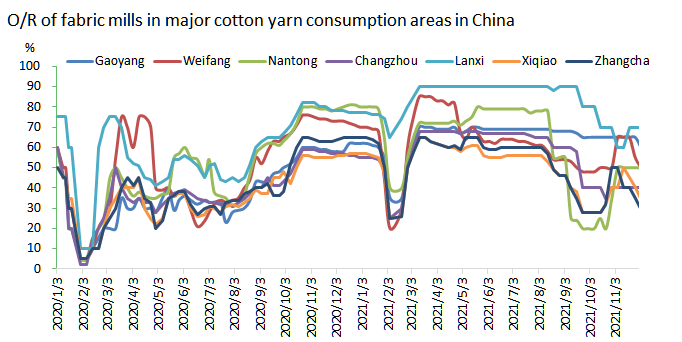

After the electricity restriction was eased in the second half of Oct, weavers raised operating rate periodically. As downstream demand weakened, the operating rate started to slide, to year’s low by now. It was heard that the operating rate of weavers in Guangdong was only around 20%, that in Nantong and Weifang 40-50%. Overall operating rate of weavers has declined to below 50%.

Dec arrivals were mostly orders in Sep and Oct, and the cargos orders in Nov will mostly arrive in Jan. Overall Dec arrivals are expected to inch up. Most traders do not place orders in recent one month and the shipment time is mostly in Dec, indicating poor market mood. With the pandemic and soft downstream demand, downstream plants are likely to take Spring Festival holidays in advance, so their pre-holiday restocking may be earlier than previous years.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price