The spring of nylon DTY

In the traditional peak season of 2024, nylon filament yarn (NFY) market wasn't as bustling as the same period last year, while filament factories faced no significant shipping pressure. In the same period last year, FDY was a definite star product, with supply shortages seen for all specifications, and orders were arranged in advance for over a month. While DTY demand was good, it still paled in comparison to FDY.

However, in 2024, the halo around FDY has dimmed slightly, while DTY has become a hot product. Even for standard specifications, it's become common for major factories to have presales. The shift in the industry "status" of FDY and DTY fundamentally comes down to their supply and demand patterns.

1. Encouraging demand growth

Looking back, the profit fluctuations of DTY are closely related to price trends on the surface, with demand having a significant impact in addition to cost influences. In recent years, the most dismal period for DTY was mainly in the second half of 2022. The release of a large amount of new production capacity, coupled with reduced consumption due to the pandemic, exacerbated the supply-demand imbalance for DTY, leading to a significant compression of processing fees to severe losses.

In 2023, as the pandemic turned a corner and nationwide travel increased, a surge in new demand, led by sun protection products, emerged. Subsequently, the growth in applications for DTY in various areas such as leisurewear, underwear, and leggings including shark pants and Barbie pants was considerable, leading to a significant increase in demand. The specifications involving DTY include many high-F products ranging from 20-70D, and there was a noticeable increase in demand in intermediate links such as air covered and conventional covered yarn. Additionally, DTY's export volume was also considerable, reaching 113,000 tons in 2023, a 23% year-on-year increase.

In 2024, the demand hotspots of 2023 were essentially continued, still mainly focusing on porous filament. The specifications closely overlapped with the popular specifications of 2021, but the market application areas were more extensive than at that time, with a breakthrough in usage. Furthermore, DTY exports grew by 13% in the first quarter, still maintaining a good growth momentum. Overall, demand growth for DTY in 2024 is not inferior to FDY, and in some areas, it may even surpass FDY, although there are no apparent new specifications or application areas showing significant volume growth.

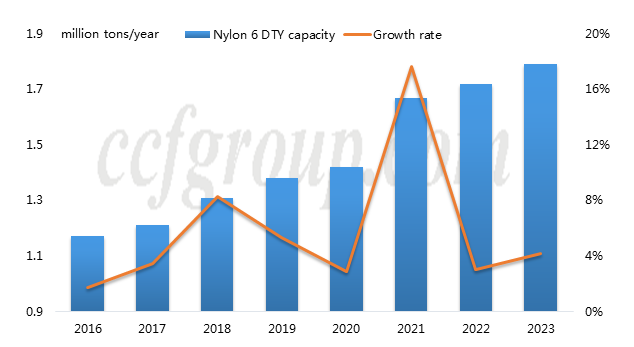

2. Supply lags behind demand

In 2024, there have been no significant new applications that have emerged for DTY market. However, DTY market seems to be in better shape than FDY market, mainly due to differences on the supply side. Due to the explosive increase in demand for sun protection products in 2023, FDY supply is more tense compared to DTY, which also prompted filament factories to plan new capacity focusing on FDY. The new capacity has been largely released from the second half of 2023 to 2024, rapidly alleviating the tight supply. In contrast, the last round of concentrated expansion of new DTY capacity occurred in 2021-2022, leading to a rapid market surplus. Although DTY demand was good in 2023, it didn't match the fervor for FDY. Additionally, the repair of processing fees for standard DTY specifications was limited, resulting in few new capacity additions from 2023 to the present. As DTY demand continues to steadily grow this year, and supply fails to keep up, the degree of supply tightness increases.

Since planning and commissioning new projects takes time, current DTY equipment is already running at full capacity. This also means that supply will be difficult to fully match demand in the short term. The current supply-demand pattern for DTY will likely persist for some time, and backlogging of high-end products will continue to be the norm this year.

Furthermore, the increase in new capacity for mid-to-high-end POY is less than that of DTY, leading to a tighter supply of POY. First, this has driven an improvement in transactions for mid-to-low-end POY, with low-end filament factories generally operating at high levels this year. In addition, nylon filament factories in South China have generally adjusted their HOY production lines to produce POY, leading to a reduction in HOY supply. Currently, HOY supply is very tight, with processing fees gradually increasing. Some mid-to-low-end POY filament factories in Jiangsu and Zhejiang have resorted to processing HOY to alleviate supply pressure, further exacerbating the tight supply situation for low-end POY. This is also the reason why both POY and HOY are in short supply in 2024.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price