MEG market: balancing bullish and bearish fundamentals with focus on unit updates

After the holiday, MEG prices experienced a rapid surge followed by a decline, largely driven by speculative purchases for late June goods. The market is currently characterized by a mix of bullish and bearish sentiments, with fluctuations lacking consistency. Despite a destocking phase and production cuts at overseas facilities, there is caution regarding the recovery of existing capacities, particularly concerning the September 2409 futures contract.

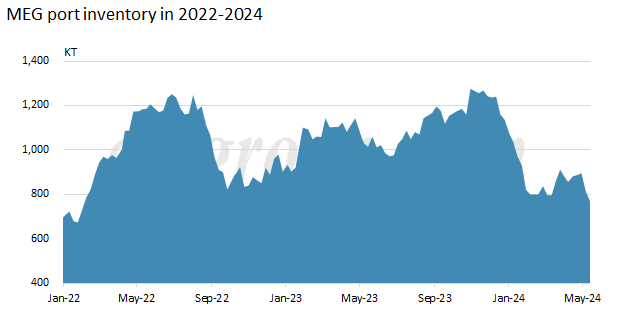

1. Ports

At the start of the month, visible MEG inventories dropped notably to approximately 810kt, signaling effective destocking at the ports with improved shipments from major trade warehouses. MEG port inventories showed decrease as well on May 13. Ship arrivals from the Middle East are reduced early in the month but will increase later. Earlier low prices prompted spot purchases by polyester factories, and robust shipments from primary ports are anticipated to continue. However, a recovery in the coal chemical operating rate has been noticeable since the start of the month, which by mid-month will likely affect port offtake demands due to increased transport to end-use markets.

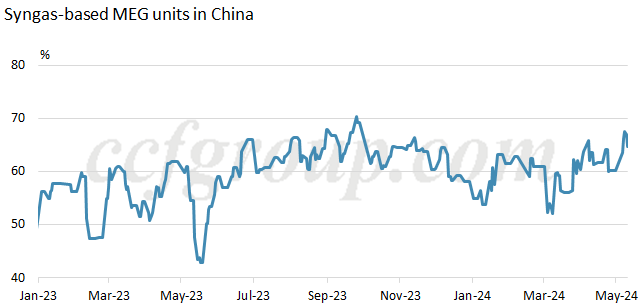

2. Plant Operation

The overall operating rate for MEG units in Chinese mainland has decreased to around 58%, with operational differences between oil-based and coal-based facilities. Coal chemical plants have resumed operations following spring inspections, aided by low coal prices and marginal profitability, except for facilities like SHCCIG Weihe Binzhou and Hubei Sanning, which are undergoing maintenance or upgrades. Oil-based facilities face significant cash flow deficits, maintaining low operational levels, with no set restart time for the ZRCC #2. Notably, Shenghong Refining has reduced some contract supplies since May, while ZPC #3's restart is delayed until late May due to equipment issues, impacting future operating rates. Additionally, some MEG plants in Saudi Arabia are reducing rates due to raw material supply issues.

Additionally, regarding related products, although the price of ethylene oxide has remained high at 7,000 yuan/mt recently, companies have reported increased pressure for sales. Demand for downstream water-reducing agents has also been weak. From January to March 2024, construction, new starts, and completions of housing projects by Chinese real estate developers all experienced double-digit declines compared to the same period last year, and the industry continues to operate at low start-up levels.

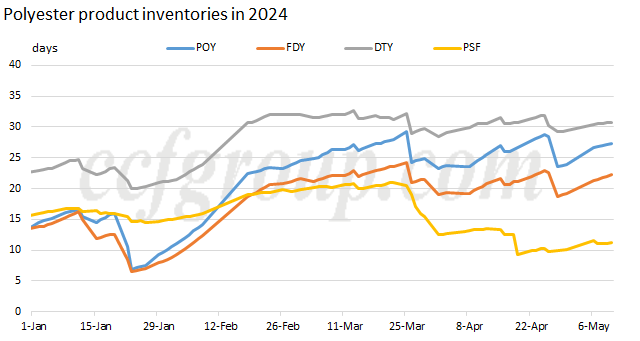

3. Supply and Demand Structure

The market's focus is on the polyester operating rate, which has been adjusted down to 89.3% by last Friday, influenced by boiler renovations and equipment failures. End-users remain cautious, mainly using up existing inventories, as polyester filament enterprises face accumulated inventory levels, returning to previous highs. The industry is closely monitoring the implementation of production cuts, with MEG destocking for May projected around 140-150kt, moving towards a slight surplus in June and July.

4. Overseas Arbitrage

From a pricing perspective, the China-Southeast Asia arbitrage window has not fully opened, but there has been interest from foreign traders in the Southeast Asian market during last week. The viability of transshipment trade remains uncertain due to costs and logistical challenges. Additionally, PRefChem is heard planned to restart its ethylene facility in June. Eyes should also rest on the status of its MEG unit.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price