Chinese listed cellulose fiber companies disclose 2023 annual report

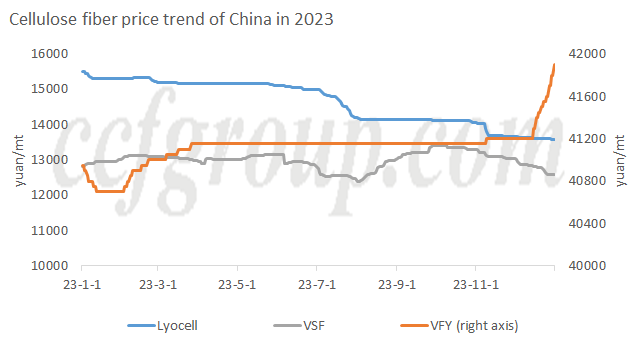

In 2023, there were many macro events, such as the bankruptcy of Silicon Valley Bank in the United States at the beginning of the year, continuous interest rate hikes by the Federal Reserve leading to sustained high interest rates, the conflict between Israel and Palestine, and so on. Despite the many unexpected events, the viscose industry chain showed relatively low volatility (except for lyocell, which experienced greater fluctuations due to overcapacity). Currently, the annual reports of relevant Chinese listed companies have been fully disclosed. Let us take a look at the details.

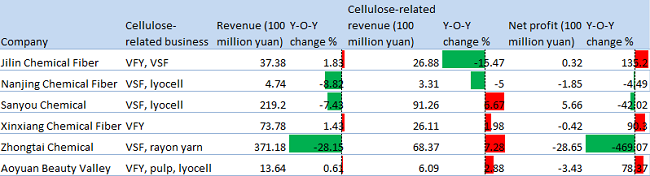

Jilin Chemical Fiber: the company is mainly engaged in the production and sale of VSF, VFY, and carbon fiber. During the reporting period, revenue increased slightly with support from carbon fiber and other business. The viscose-related business shrank due to a significant decrease in the production and sales volume of VSF, as the VSF line was operated as contract processing throughout the year. However, revenue from other business increased significantly, possibly stemming from contract processing business. The production of VFY was 68,642 tons (an increase of 7,935 tons year-on-year), without production of VSF (a decrease of 42,948 tons year-on-year). The sales volume of VFY and VSF was 69,656 tons and 376 tons respectively. The capacity utilization of VFY and VSF was 85.8% and 81.47% respectively (an increase of 9.92% and 11.26% year-on-year). Additionally, the company has expanded VFY capacity by 10kt/yr, with civil construction completed and equipment installation underway.

Nanjing Chemical Fiber: the company mainly produces and sells VSF and lyocell. During the reporting period, the production and sales volume of VSF was 30,617.19 tons and 30,424.06 tons respectively (an increase of 2,090.09 tons but a decrease of 28.17 tons respectively year-on-year), with equipment maintenance arranged by Jiangsu Jinling. As for lyocell, the company is still working on achieving production standards, and there were no sales revenues during the reporting period. In addition, in the viscose sector, the company is developing differential products such as dispersible ultra-short fibers (including filament tow).

Sanyou Chemical: the company's main products are VSF, soda ash, PVC, caustic soda, and silicone. During the reporting period, the production and sales volume of VSF was 751.4kt and 746.8kt respectively (an increase of 101.2kt and 83.2kt respectively year-on-year), with the flame-retardant fiber sales volume increasing by 116%. The capacity utilization of VSF was 96.34%, and the net profit for the sector was -211 million yuan (an increase of 359 million yuan year-on-year).

Xinxiang Chemical Fiber: the company mainly produces and sells VFY and spandex. During the reporting period, both the spandex and VFY business segments saw revenue growth. The capacity of VFY was 90kt/yr, with an additional 10kt/yr under construction. The production and sales volume was 67,804 tons and 68,794 tons respectively (an increase of 1,022 tons but a decrease of 629 tons respectively year-on-year). The capacity utilization of VFY was 87.98%. Benefiting from lower shipping costs and a higher US dollar exchange rate, the gross profit margin of biomass cellulose filament increased by 5.53%, leading to a gross profit increase of 152 million yuan.

Zhongtai Chemical: the company's main businesses are chlor-alkali chemical and viscose textile. During the reporting period, the capacity of viscose fiber and rayon yarn was 880kt/yr and 3.2 million spindles respectively. The operation rate was 64.99% and 85% respectively, with production of 569kt (an increase of 13.39%) and 319.9kt (an increase of 20.54%) respectively, and sales volume of 208.5kt (a decrease of 10.17%) and 318.1kt (an increase of 29.94%) respectively.

Aoyuan Beauty Valley: the company mainly engages in bio-based fibers (lyocell and VFY) and medical beauty business. During the reporting period, the auditor issued an unqualified audit report with the significant uncertainty paragraph of continuing operations. The production of VFY and lyocell was 10,121.26 tons and 13,593.24 tons respectively (an increase of 575.24 tons and 5,183.96 tons year-on-year), with sales volume of 9,107.44 tons and 13,344.31 tons respectively (a decrease of 771.02 tons and 3,052.21 tons respectively year-on-year). The capacity utilization of VFY and lyocell was 67.48% and 33.98% respectively.

In summary, in 2023, the revenue of cellulose enterprises showed a mixed trend of increase and decrease, with three companies experiencing no significant growth (Jilin Chemical Fiber, Nanjing Chemical Fiber, and Aoyuan Beauty Valley). Revenue in the cellulose sector generally increased, with only Jilin Chemical Fiber and Nanjing Chemical Fiber experiencing a year-on-year decline. In terms of profits, companies generally suffered losses, with Zhongtai experiencing significant losses.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price