Nylon semi-dull HS chip price surges on strong fundamentals

Recently, there has been a particularly tight supply of semi-dull HS (high-speed spinning) chips. High-end chip is still mainly traded by contract, and mainstream manufacturers have no spot supply available, and even in cases where there is some spot availability, the amount depends on their relationships with the supplier. Finding any quantity is considered good, with sellers setting the prices and buyers having minimal room for negotiation. The lower-end HS chip market primarily relies on spot trading, and due to the overall shortage in the semi-dull HS chip market, spot prices have been increasing continuously, leading to an independent market trend.

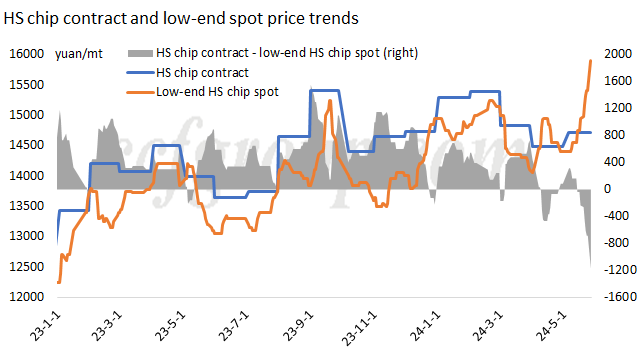

1. Low-end HS chip spot prices significantly exceed high-end contract prices

Historically, low-end HS chip spot prices have generally been around 300-500yuan/mt lower than high-end HS chip contract prices. During periods of relatively abundant supply, the difference can expand to 800-1000yuan/mt or more. In tighter supply situations, the price difference narrows or becomes nearly equivalent. It's rare to see spot prices in the lower-end market surpassing those in the high-end market. However, in April 2024, there was a surge in lower-end HS chip spot prices, exceeding high-end contract chip prices by 400-600yuan/mt. Since May 13, lower-end spot prices have consistently risen, with price rising from 14500-14600yuan/mt to the current highest 15900-16000yuan/mt, 6 months payment delivered. Meanwhile, the high-end chip contract price in May is around 14665-14765yuan/mt, resulting in a nearly 1,200yuan/mt difference, clearly indicating an inversion in high and low-end prices.

Continuously seeing lower-end spot prices surpassing high-end contract prices in the short term reflects the sustained tightness in the supply of semi-dull HS chips and the robust trading resilience in the spot market under this supply-demand structure.

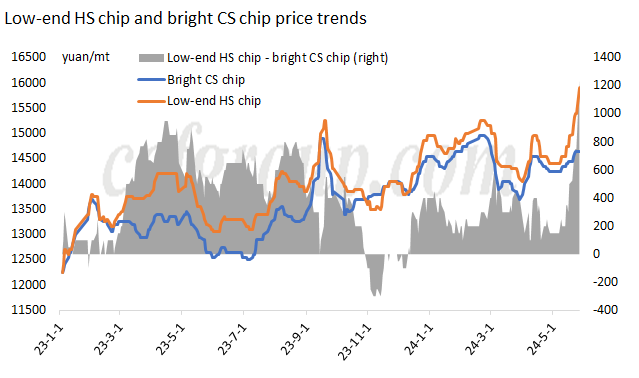

2. The increase semi-dull HS chip spot evidently larger than CS chips

The spot market trend for HS chips is relatively strong, a comparison with CS chips' trend highlights this fact. Comparing spot prices of bright CS chips with low-grade HS chips, last year, CS chip market experienced oversupply, leading to a price difference of about 400-800yuan/mt compared to HS chips. This year, as CS chip demand improved and supply and demand rebalanced, the overall market moved out of a low period, causing the price difference with low-grade HS chip spot prices narrower to around 200-400yuan/mt. However, in recent days, the low-grade semi-dull HS chip spot prices have surged, resulting in a price difference of over 1100yuan/mt, reaching a new high for this year.

The main cause is the insufficient increase in supply compared to demand.

Why has the spot market for semi-dull HS chips become so tight, and why is the spot market price for lower-end chips significantly higher than high-end contract prices? The main reasons are as follows:

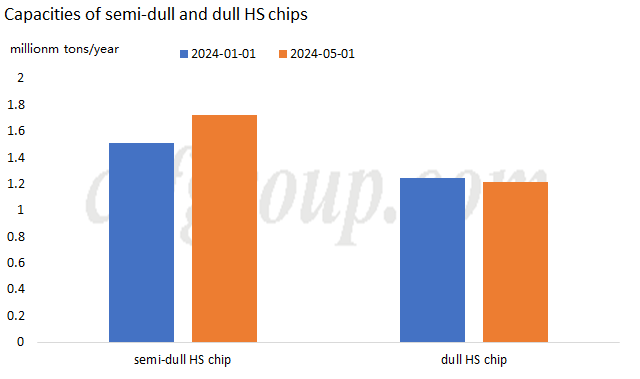

1. In 2023, the growth in demand for dull HS chips was more pronounced, prompting polymerization plants to switch production to dull HS chips. This production shift continued until January 2024. However, the concentrated and excessive switch to dull HS chips resulted in rapid oversupply, leading to a gradual reduction in effective production capacity for semi-dull HS chips and the subsequent tightening of supply.

2. In 2024, the demand side has continued the strong growth momentum seen last year. While there isn't a standout area with a dominant demand, there is steady growth across various sectors. There is demand for semi-dull and dull chips in various areas, and the demand distribution is not significantly biased.

3. With the tightening supply and continuous demand growth, the shortage of semi-dull HS chips has become more pronounced, and the pressure on dull HS chips is increasing daily. Therefore, since March, the operation of polymerization plants switching from dull HS chips to semi-dull has gradually increased. In addition, with some idled equipments restarting, as of now, the effective production capacity of semi-dull HS chips has increased by over 200,000 tons/year compared to the beginning of the year (including Hengyi, Highsun, Fangyuan, Yongtong, etc.). However, the market still faces a supply-demand imbalance primarily because demand growth is more significant than chip production growth. (See consumption growth in insight " The spring of nylon DTY".)

4. As for why low-end spot chips are more dominant in price compared to high-end contract chips, there are mainly two reasons. Firstly, the high-end market is mostly dominated by contract trading, with prices adjusting along with the contract CPL. Even if some high-end manufacturers provide spot prices, spot availability is scarce. Low-end semi-dull HS chip factories mainly engage in spot trading. When market supply is significantly tight, spot prices deviate from contract prices, leading to a continuous increase in the price difference between the two. Secondly, the customer base for low-end spot chips mainly consists of small nylon filament factories in Jiangsu and Zhejiang provinces. These manufacturers rarely sign raw material contracts, and this year, medium and large high-end filament factories primarily focus on producing differentiated products with higher production efficiency. Orders for conventional POY and DTY coarse filament products are gradually flowing to smaller factories, leading to high operating rates in these small factories and improved profits. Therefore, as the prices of low-end spot chips continue to rise, nylon filament small factories are compelled to purchase. Moreover, due to acceptable profits and the ability to temporarily bear short-term costs, pursuing price increases further drives up the prices of low-end spot chips to the limit.

Conclusions:

a. Can the short-term supply of semi-dull HS chips be alleviated? It seems challenging considering new production capacity is scarce in the next 1-2 months. However, with an oversupply of dull HS chips and the significant profitability of semi-dull chips, polymerization plants will inevitably accelerate the switch from extinction or brightness devices to semi-dull operation, which may result in increased production capacity from various plants in 1-2 weeks.

b. How long can the current momentum of spot prices be sustained? The author believes it won't last too long. High processing fees are accelerating the concentration of polymerization plant line changes. When supply and demand reach near equilibrium, spot processing fees are expected to rapidly return to normal.

c. Will the strong performance of semi-dull HS chip spot prices drive a significant increase in CPL? Since semi-dull spot sources are mainly low-end and account for a small proportion of the market total, the direct impact on driving up CPL is expected to be limited.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price