Nylon 66 chip market outlook for Q3 2024

Since the latter half of April, nylon 66 chip market sentiment has gradually weakened, downstream factories are purchasing on demand, and chip prices after the Labor Day holiday continue to trend slowly downwards. So, how will the market trend for nylon 66 chips be in the future? We will mainly analyze it from the following points:

I. Pressure on the cost side

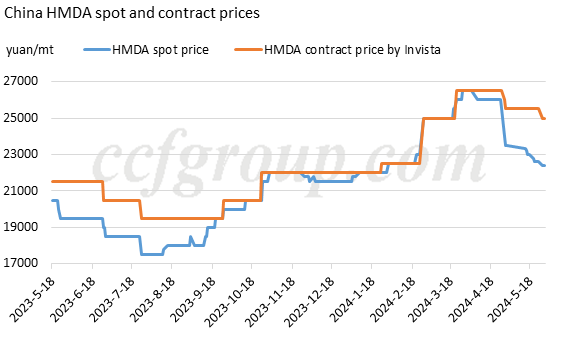

1. Key raw material, HMDA cost declines signficantly

In terms of mainstream factory quotations, in June, Invista's HMDA contract price was released at 25,000yuan/mt, a decrease of 1,500yuan/mt from the previous month. The deep decline in HMDA prices during end-Apr to early May was mainly due to the eased supply tension, as Tianchen Qixiang has restarted its HMDA production and formed effective supply to the market, with mainstream transactions around 23,000yuan/mt, and some low-priced orders appeared. With weak downstream chip demand, HMDA prices lack sufficient support.

Looking back to the beginning of the year, HMDA prices have been rising up significantly, with Invista's contract price rising from 22,000yuan/mt to a highest at 26,500yuan/mt in end Apr, and spot prices rising from 22,000yuan/mt to as high as 26,000yuan/mt, up around 4,000-4,500yuan/mt. But its downstream nylon 66 chip only rose from 19,700yuan/mt to 22,600yuan/mt, up around 2,900yuan/mt.

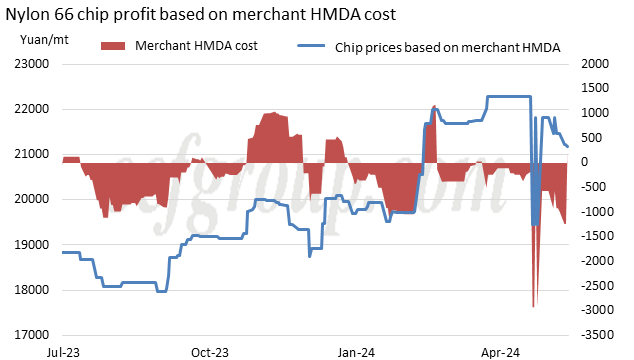

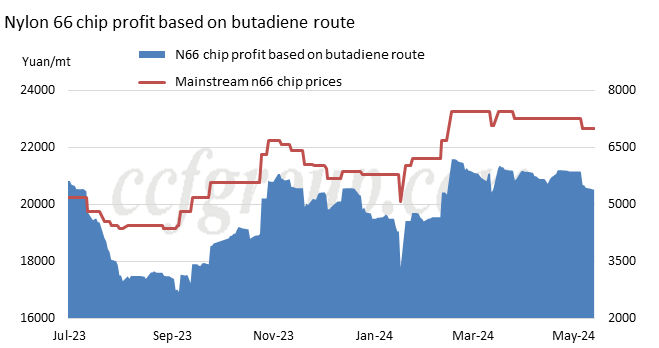

The above chart shows that, nylon 66 chip plants, who are not integrated with raw material production and need to purchase HMDA from the market, has been struggling around the break-even line, since the beginning of this year. But this situation would be much better for chip plants integrated with upstream. The chart below shows the butadiene-route HMDA production cost, which was represented by Invista, and these part of polymer plants are making lucrative profit. It also shows that the profit margin of nylon 66 industrial chain has been concentrated in HMDA part.

2. Adipic acid oversupply situation improves slightly

The operating rate of adipic acid plants has decreased slightly, and the situation of oversupply has slightly improved.

Currently, based on the industry's average level, the loss of producing one ton of adipic acid is around 1,300yuan, so the operating rate of AA is relatively low. Many small and medium-sized factories choose to operate less or not at all to limit losses. However, recent maintenance additions in Xinjiang Tianli and Liaoyang Petrochemical have slightly eased the oversupply situation in the market, curbing the previous downward price trend.

In conclusion, it is expected that AA prices will stabilize or even slightly increase, but constrained by the high operating prices of raw materials, profits will still be under pressure. Compared to AA, the price decrease of HMDA is more significant. Overall, it is anticipated that the future cost of chips will stabilize with a slight decrease.

II. Longer supply in chip market

1. The chip operating rate has increased slightly.

Currently, there are not many maintenance plans of nylon 66 plants for May and June, and Tianchen's 40,000-ton production line has resumed full production, increasing the overall operating rate from 70% to 75%.

2. There is a considerable amount of new chip production capacity.

Aside from the additional supply, the increase mainly lies in new line investments. According to research, it is expected to see additional 310,000 tons of new chip production capacity by June 2024, with at least an additional 80,000 tons planned by the end of the third quarter. While actual production may be delayed due to various factors, the supply is noticeably leaning towards being ample. It is expected that the actual new production will exceed 200,000 tons in the year of 2024, representing a rapid growth rate. In addition to the production lines under construction, the planned chip production capacity is also significant.

It is predicted that the chip market supply will gradually move towards oversupply after June.

III. Weakening demand compared to the previous period

In terms of downstream rigid demand, demand for modified plastics, industrial filament, and textile filament is relatively stable. While there is growth in demand and capacity expansion, it is slower compared to the expansion of chip production capacity. Therefore, with speculative demand, downstream players generally have a bearish outlook. Chip prices are constrained by the off-season effect, with little short-term demand growth, and factory distributors find it challenging to boost purchasing intentions. With a mainly wait-and-see attitude and insufficient inventory intentions, the market is primarily weak due to the lack of demand aligning with the orders put forward.

Therefore, considering the above points, the price trend for nylon 66 in the upcoming quarter is expected to remain weak with a continual decline, a higher probability of a gradual decrease in production rates, and the market picking up awaiting the arrival of the traditionally strong season in September and October.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price