PTMEG additional supply evident, price declines in H1 2024

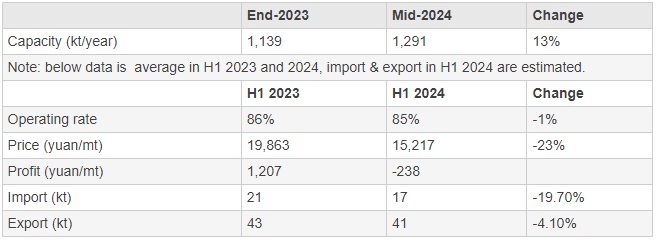

In the first half of 2024, the release of PTMEG production capacity increased. By the end of June, the annual production capacity of PTMEG in Chinese mainland has reached 1.291 million tons/year, an increase of approximately 13% compared to the end of 2023, with a net increase in annual capacity of 152kt/year.

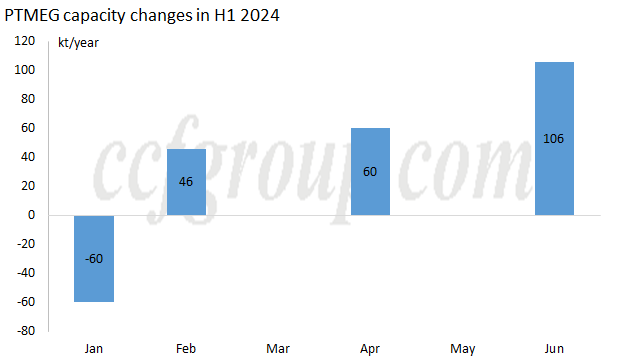

Looking at the changes in PTMEG production capacity in H1 2024, the release of new capacity was mainly concentrated in the second quarter. In the first quarter, due to the temporary reduction in capacity of a long-standing unit, the net production capacity decreased. In the second quarter, capacity expansion significantly increased with the commissioning of new projects from Hengli Petrochemical, Huaheng Energy, and Junzheng Chemical, leading to a notable increase in capacity.

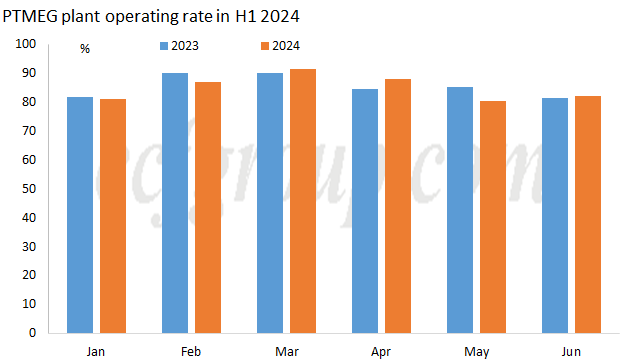

The industry's average operating rate in the first half of the year was around 85%, a decrease of 1 percentage point compared to the same period last year. Although capacity expansion in the industry increased, as it was mostly concentrated in the second quarter, the average operating rate in the first half of the year was almost flat year-on-year. Sequentially, planned maintenance and minor production reductions increased in the second quarter compared to the first quarter.

Under the expansion of capacity and high operating rate, the preliminary statistics showed that the total production of PTMEG in the first half of the year was approximately 555,000 tons, a year-on-year increase of about 29%. Not only did the supply increased significantly in the first half of the year, but demand also increased noticeably. Incompletely accounting for demand performance in the first half of the year, demand for PTMEG also saw a year-on-year increase of nearly 30%.

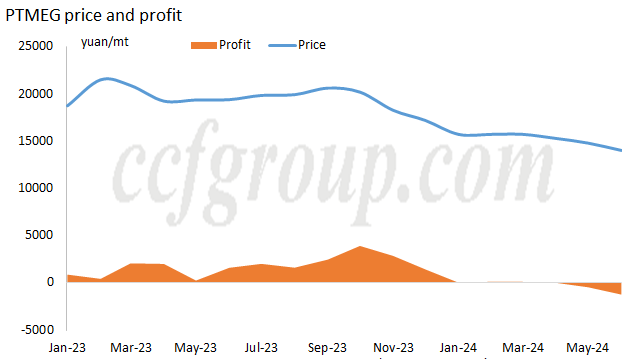

With the increase in supply altering the supply-demand relationship, PTMEG market prices continued to decline, directly falling below the cost line.

After two years of decline, PTMEG prices had eroded its profits. In the first quarter, PTMEG remained profitable in the spandex industry chain, but started facing losses in the second quarter, which deepened by June. With the exception of a few high-end brands maintaining higher prices, most domestic sources were priced around 13,500-13,700yuan/mt. The average price index of PTMEG in the first half of the year was around 15,217yuan/mt, a year-on-year decrease of about 23%.

As prices fell, the pressure of losses increased. The industry saw minor profits in the first quarter, but with continuous price declines in the second quarter, prices began to fall close to the cost line. By June, the average loss per ton was around 1,200yuan. Some sources, especially lower-priced ones, started facing cash cost pressures. The average profitability in the first half of the year also showed slight losses, but supported by production and sales volume increases, actual operations in the first half of the year showed slight profits. The industry's competition is intensifying amidst increasing supply and imbalanced supply-demand dynamics, which is likely to lead to price adjustments near the cost line.

According to customs data on PTMEG imports and exports from January to May, as well as estimated data for June, both imports and exports of PTMEG in the first half of the year are expected to decrease. The reduction in import volume is particularly significant, influenced by increased domestic supply and substantial price declines. Import volume in the first half of the year is expected to be close to 17,000 tons, a year-on-year decrease of approximately 19.7%. While exports showed a slight rebound compared to the second half of 2023, it is expected to have a small year-on-year decrease. The total export volume in the first half of the year is around 41,000 tons, a year-on-year decrease of about 4.1%.

PTMEG industry operations data in H1 2024

Looking ahead to the second half of the year from a fundamental perspective, the supply-demand situation remains weak. Supply is expected to continue releasing, with the possible commissioning of about 166,000 tons/year new units pending in the second half of the year. The cost side has strong support under the pressure of comprehensive losses among the industry, even starting to experience cash flow losses. The space for price adjustments is very limited. The market in the second half of the year is expected to make narrow adjustments at low levels under competition, with a potential overall decrease in the industry operating rate.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price