Nylon filament demand forecast in H2 2021: still cautious

Nylon filament market performance in the first 7 months of 2021 has been basically healthy. Even in the traditional slack season of June and July, only the conventional products appeared to be slack, while sales of the hot-sold products have never been dull.

The peak season is coming closer, and part of downstream demand is expected to recover in late August. Before the peak season truly comes, we will review the supply and demand performance of nylon filament in the January-July 2021.

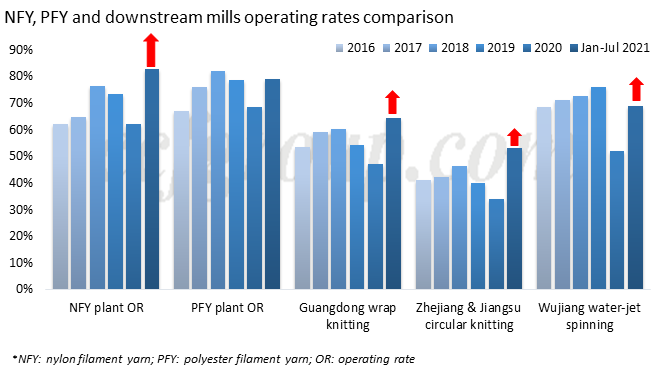

Supply: NFY and downstream plants' run rate in slack season higher year on year

Nylon filament plants have been running at higher rates in 2021. In January-July 2021, the average operating rate of nylon filament yarn (NFY) plants has been assessed above 80%, 20.6 percentage point higher than the same period of 2020, and 9.5 percentage point higher than that of 2019. In comparison with polyester filament yarn plants, which has just recovered to the similar rate in 2019, while nylon has evidently grown higher than that of 2019.

Nylon downstream fabric fields have similar growth in Jan-Jul 2021, as the comprehensive operating rate of nylon downstream has increased 16-19 percentage point than the same period of 2020.

Seeing the growth compared with Jan-Jul 2019, the average run rate in circular knitting mills has increased 13-14 percentage point, and that in warp knitting mills has lifted 10 percentage point. Although the overall run rate in water-jet spinning mills has lowered 7 percentage point from 2019, it is not a nylon dominated market, and the actual situation of nylon-based water-jet mills is good, and their run rate is also higher than that in 2019.

The rising operating rate in NFY plants has been matched with the growth in the various downstream sectors. Particularly, the intensive expansion in the circular knitting mills has contributed to a much higher consumption of nylon filament this year. It is why nylon filament mills' operation has recovered more than that of polyester filament plants.

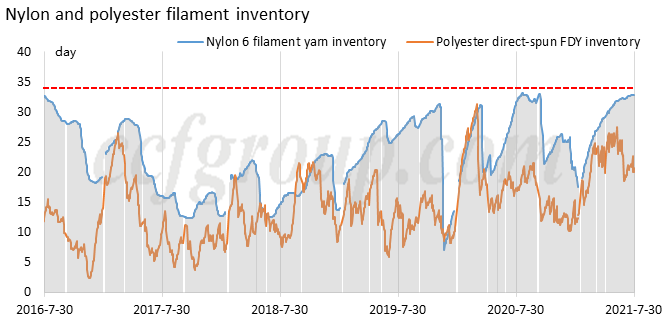

Supply: NFY inventory also higher year-on-year

With NFY plants operating continuously at highs, nylon filament inventory has been accumulated. By the end of July, NFY inventory is assessed at 33 days, a yearly highest rate and higher than the same period in the past two years (31.8 days in 2020, 26.3 days in 2019). The similar condition is seen in polyester filament plants as well.

However, NFY plants have not cut production in the May-July, as they usually do in the previous years, even when the inventory has built up to a yearly high rate. This strengthens the point that the consumption of nylon filament by downstream weaving and knitting mills has been very robust in 2021.

Actually, NFY production and demand from fabric has been smooth so far. Supply and demand of NFY has been kept in a balanced structure.

Then, is supply and demand also balanced at the end of the textile industrial chain?

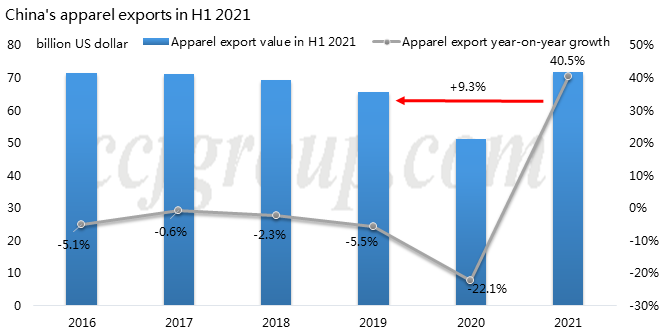

Demand: export demand grows vigorously

As an end use market of the textile industry, apparel export was evidently impacted by the COVID-19 pandemic in 2020. In 2021, the world economy has formed a new normal, as the pandemic has periodically broke out around the world. Apparel production in Southeast Asia has been severely damaged by the pandemic, and part of its export orders have shifted to China.

In the first half of 2021, China's apparel export has grown by 40% year-on-year, and 9.3% compared to the same period of 2019, which is basically in line with the increase in nylon filament yarn plants' operation rate increase (9.5% higher than 2019).

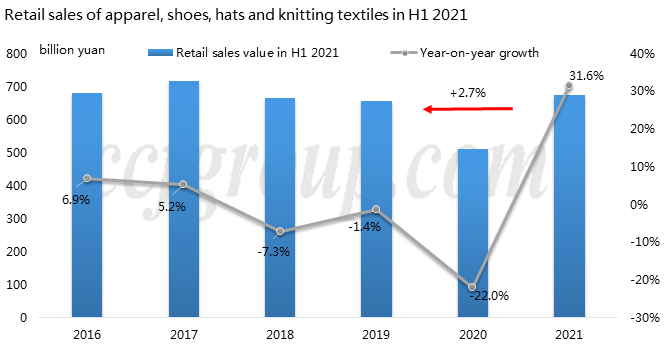

Demand: China domestic demand recovers steadily

Apart from export orders, China domestic demand for apparel has apparently recovered. In Jan-Jun 2021, the sales of apparel, shoe and hat has grown by more than 30% year-on-year, while the increase is just 2.7% compared with the same period of 2019.

During this period, the price index of apparel, shoes and hats did not fluctuate much. It can be seen that China domestic demand for apparel has limited growth in addition to repairing the gap in 2020, which is far less than the growth rate of upstream supply.

Demand in coming peak season expectable, but forecast for H2 2021 still cautious

It can be seen that supply and demand is basically balanced between nylon filament yarn and downstream fabric market. NFY inventory is accumulated in filament plants, while not high in downstream. The production and sales in NFY plants have been kept a healthy balance. That is especially the case that NFY plants have been operating at high rates over the first 7 months in 2021. It has set a solid base for the bullish outlook for nylon filament yarn market toward peak season in September.

However, there is oversupply risks from fabric to end user's consumption. The pandemic influence is swiftly changing in Chin and the world and high freight rate in 2021 is a major hinder to export trading. In addition, finished fabric stock has accumulated, particularly for the fast expanding circular knitting sector, and it may weaken demand in peak season in September-October or shorten the peak seasonal sales. Therefore, we stay cautious in forecasting end user's market toward October and forward.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price