MEG finds support from buying with price lower than MTD average

Due to high inventory of grey fabric, production losses and scarce new orders, more water-jet looms in northern Jiangsu were closed and some large-scaled home textile fabric producers closed their machines. Up to August 13, Loom operating rate in Zhejiang and Jiangsu fell to around 74%, and the rate may likely decrease further.

With the continuous weakness in end-user market, some polyester plants cut output. Polyester polymerization rate was estimated at around 89% Monday and may further decrease to around 87.5%. Looking ahead, eyes could rest on the reduction implementation of Hengyi and Xinfengming. Forecast for August polyester polymerization rate has been revised down, and the supports to MEG market weakens.

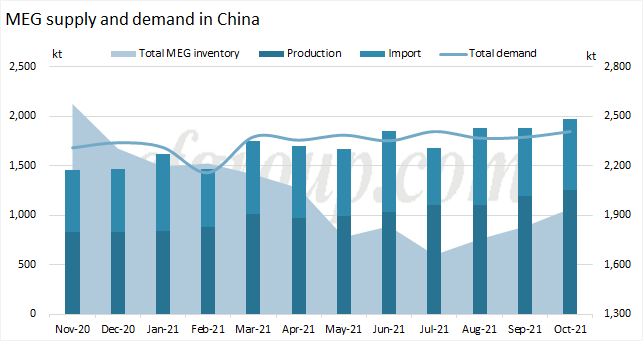

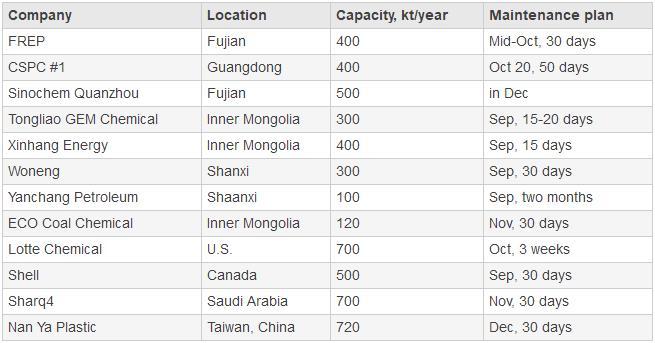

In supply side, Hengli Petrochemical and PetroChina Sichuan Petrochemical closed their plants shortly and ECO Coal Chemical cut operating rate for days. Restart of Weihe Binzhou Chemical was postponed. Recovery in MEG plant operating rate was less than expected. China domestic output was estimated at around 1.1 million tons in August, broadly flat with in July.

Import cargo arrivals will gradually decrease since August 20 and the recovery in port inventory would be limited. Meanwhile, supply outside China remained tight due to plant shutdowns and rate cut in Saudi Arabia. As a result, China's September MEG import will remain low. Total MEG inventory is expected to go up, but with limit increase. Given the low inventory level in East China main ports, MEG fundamentals are neither stronger nor weaker.

Looking ahead, some producers in China have maintenance plans and supply outside China may hard to see effective recovery, so China's MEG imports will keep low. Around mid-September, Hualu Hengsheng, Weihe Binzhou and Tianye III are expected to come back to the market. In terms of new capacities, eyes could rest on Gulei, Huayi and Haoyuan. Gulei Petrochemical is expected to commission its MEG plant with its own ethylene in late August. Guangxi Huayi has started its 200kt/year syngas-based MEG unit in Qinzhou in the second week of August but has not achieved MEG products yet.

After the sharp fall, the current MEG price is much lower than the month-to-date average. Traders are likely to buy at low prices. Eyes could rest on polyester output cut and MEG supply recovery.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price