Market review of PFY market in 2021

Price shivered and cost and cash flow moved up

Prices of PFY saw 3 times of sharp ups-and-downs in 2021 and the increment was bigger in early-2021 and end-2021, which was highly consistent with the prices of chemical industry.

The first increased appeared after the Spring Festival holiday. Cost side climbed up with recovering demand in Feb coupled with decreasing supply of feedstock caused by the cold snap. Price of POY150D/48F increased by 2,000yuan/mt to 8,000yuan/mt. PFY plants saw rapidly recovering cash flow and resumed operation rapidly after the Spring Festival holiday. However, PFY price headed south later with inadequate demand and mounting stocks. Leading PFY companies had high concentration ratio of stocks and capacity and discounted price periodically for promotion. Price of POY150D/48F reduced to above 7,000yuan/mt.

The second uptrend appeared in mid-2021. Speculative demand for PFY was good after the Dragon Boat Festival (early-Jun) and buyers in Guangdong purchased the earliest. With rebounding cost, speculative demand and some export demand was pulled forward in Jun. Stocks of PFY apparently dropped and PFY price increased in late-Jun. Price of POY150D/48F rose by 1,000yuan/mt to 8,000yuan/mt but declined to around 7,000yuan/mt in Aug due to weaker demand.

The third increase emerged in Sep-Oct. Some PFY plants were required to control energy consumption from Jul, especially those in Hangzhou, Zhejiang, but strict and large-scale energy consumption appeared in Sep-Oct mainly caused by tight supply and surging price of energy like natural gas and coal. Prices of PFY hit new high amid shrinking supply and increasing cost, with POY150D/48F up to 9,000yuan/mt. During this period, more DTY and fabric mills shut down compared with PFY factories. That meant the shrinkage of demand was bigger than that of demand, which laid foundation for the later reduction. At the end of 2021, PFY prices rapidly decreased due to muted demand and collapsing cost, with POY150D/48F down to below 7,000yuan/mt.

In the second half of year, soaring price of crude oil, natural gas and biomass pushed up the electricity fee and price of oil agent. The cost of PFY was revised up in 2021, with that of POY150D up by 100yuan/mt to 1,250yuan/mt and that of FDY up by 200yuan/mt to 1,750yuan/mt.

Based on the adjusted cost, the cash flow of POY150D/48F averaged at 370yuan/mt in 2021, up by 300yuan/mt on the year, and that of FDY 150D/96F was around 30yuan/mt, basically flat with 2020. The profit of POY was higher than that of FDY.

Capacity and production still saw high growth

New direct-spun PFY capacity rose by 3.4 million tons or 9% in 2021. Among this, POY accounted for 68% and FDY took up 32%. By the end of 2021, effective direct-spun PFY capacity increased to 37.17 million tons, mainly contributed by Hengyi, Xinfengming and Hengli, accounting for 39.7%, 25.6% and 17.6% of the total new increase. PFY plants ran at high capacity at the beginning of year but gradually decreased later. The PFY production was estimated to rise by 12% to 35 million tons in 2021.

Demand presented strong at first but weakened later

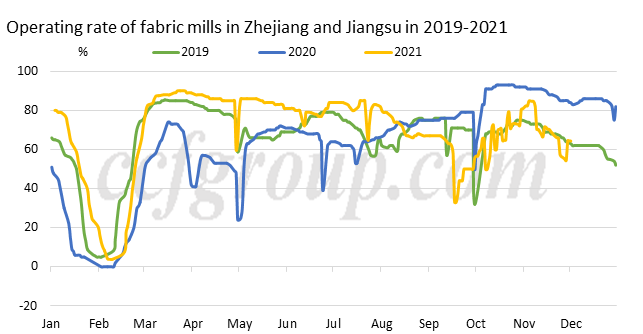

Demand for PFY was good in the first quarter of 2021 like Q4 2020 when speculative demand was moderate due to rising cost and overseas demand was tolerable amid moderate macro environment and the production suspension in Southeast Asia amid the pandemic. PFY companies ran at high capacity. In the second quarter, PFY and downstream plants kept running at high capacity but stocks extended higher when domestic plants were active in hoarding up stocks in expectation of good demand in the second half of year and some export orders were placed in advance due to freight issue and demurrage. From the third quarter, plants on the polyester industrial chain slashed run rate with weaker domestic and export demand and the Dual Control of energy consumption, especially in Sep-Oct. Under such circumstance, the inventory burden of the polyester industrial chain was mitigated. PFY plants ramped up run rate. However, PFY plants reduced run rate in Dec when demand remained muted after plants in Southeast Asia resumed operation and high sea freight and exchange rate issue dampened orders.

Demand may be pressed in 2022

Supply of PFY is expected to rise stably in 2022 and new capacity expansion does not reduce. The growth rate of demand may decrease on the year.

On one hand, China will still face the external import risk of the epidemic in 2022, and the emergence of local outbreaks will still disturb part of the demand. In addition, with the increasing downward pressure of the economy, the slower increase of residents' income and the decline in consumption power and willingness will continue. Therefore, the growth of domestic demand for textile and apparel may remain low in 2022.

On the other hand, with eased pandemic outside China, the production of textiles and apparels has recovered in Southeast Asia. That means the replacement effect of China to Southeast Asia may weaken. Overseas buyers may show falling demand for replenishment in 2022 compared with 2021 with high sea freight and some replenishment in 2021. Exports of textiles and apparels may fall from high growth rate in 2022.

High sea freight and demurrage will change the procurement peak season of export orders in 2022. The 19th Asian Games Hangzhou 2022 is expected to disrupt the production and replenishment tempo of PFY. Other factors like the spread of pandemic and energy consumption policy will also impact the cost, supply and demand of PFY. There are many uncertainties on PFY market in 2022.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price