Is the peak season of imported cotton yarn coming?

Since the second half of December, sales of spot imported yarn mills in Guangdong, Nantong and Shandong have all turned better, and the prices have risen. Trader’s origin second-lined Pakistani siro-spun carded 10S in Guangdong has risen from 22,500yuan/mt at the end of last month to 23,600yuan/mt, after-tax, up 1,100yuan/mt in two weeks. However, the downstream weavers who planned for the holiday in end-Dec and early-Jan now may take holidays on Jan 15. Therefore, traders were generally not optimistic about the outlook around mid-Jan; but from the performance of the current market, the overall price has risen to varying degrees, so is the peak season of imported cotton yarn coming?

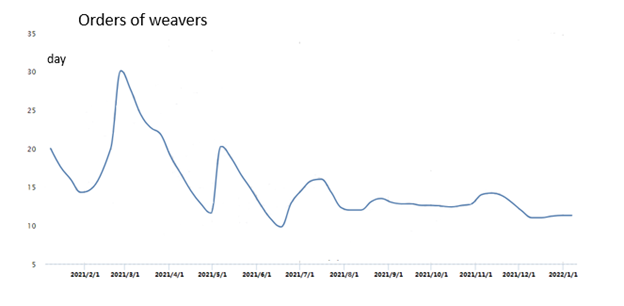

From the recent orders of cotton grey fabric mills, there were new small post-holiday orders. Compared with the current spot market with relatively good trading mood, the downstream post-holiday orders have not improved significantly. Although the post-holiday finished product inventory slightly reduced, the overall was still high, available for one month. At the same time, the downstream weavers basically were shutting down for Lunar New Year holidays, so operating rate continued to decline. There were also other factors that entered into the market.

For a start, limited spot inventory of traders and their reluctance to cut prices.

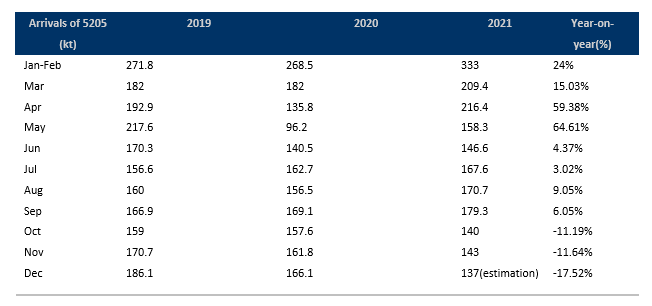

The spot has been lower than the forward since the second of 2021. Arrivals of cotton yarn have continued to decline since Oct, and that in Oct and Nov was the lowest for the whole year, down 11.19% and 11.64% respectively year-on-year. However, the arrivals in December is estimated at 137,000tons, so there is a big decline in cotton yarn arrivals in Oct-Dec. After slow destocking within several months and underselling of some traders in order to withdraw funds at the end of December, the overall spot inventory of traders was at a low level at the beginning of 2022. Just at this time, Indian cotton price has risen sharply, and the price of Indian cotton yarn has followed up. At the same time, the quotation of Vietnamese yarn, Indonesian yarn and Uzbekistani yarn has also risen to varying degrees, so traders were reluctant to undersell goods and those with low stocks withheld offering or quoted up.

Secondly, due to difficulties of replenishing forward imported yarn, traders shifted to seek for domestic sources.

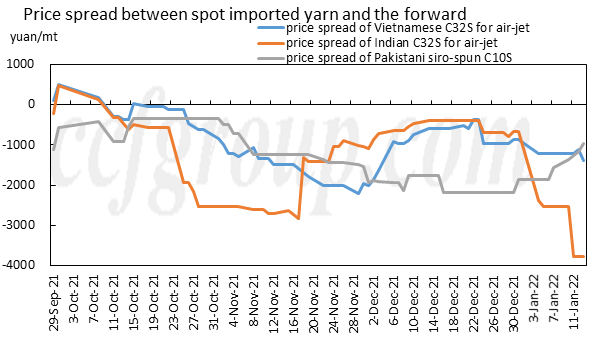

From the recent price spread, the lowest price gap was near Dec 24, mainly because foreign yarn mills short-term quoted some low-priced shipments, mainly the Vietnamese yarn, Indian yarn and Uzbekistani yarn. During this period, some brands of cotton yarn saw flat price spread or even a little profit, and domestic traders replenished goods slightly.

After that, Uzbekistani and Vietnamese yarns mills rapidly raised their quotations. The Indian yarn rose rapidly in line with Indian cotton, and the replenishment window was only about four or five days. But some traders were pessimistic about the outlook, so they were more hesitant about replenishment. As a result, they did not seize the opportunity of forward imported yarn replenishment but chose cheaper domestic spot sources for next year. Recently, some traders who were bullish on the post-holiday market built up stocks.

Thirdly, downstream weavers withdrew capitals late, so the replenishment plan postponed.

In earlier stage, the weavers basically purchased for pressing demand, and the overall inventory of yarn was limited, so it was necessary to prepare goods for consumption in the coming year. Recently, the trading sentiment in Guangdong and Shandong has improved, and the weavers in these areas have withdrawn capitals late, so replenishment continued.

In conclusion, market players mostly hold bullish expectation to post-holiday market. But whether it can usher in a real bull market in the imported cotton yarn market after the Spring Festival holidays needs to further observe the downstream orders and the destocking of finished product inventory in textile mills. At the same time, pay attention to the macro risk: whether the Fed raising interest rates to curb inflation will drive commodities into a bearish market and then affect domestic cotton yarn prices, and whether the replenishment will curb the demand for cotton yarn after the holidays in the short term.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price