Interpretation of USDA's Jan supply and demand report on cotton

The U.S. Department of Agriculture (USDA) released the global cotton supply and demand for January. The main adjustment in this report is a significant reduction in the consumption for the 2023/24 season, resulting in global ending stocks shifting from a decrease to an accumulation. Overall, the adjustments lean towards a bearish outlook. However, despite this, the cotton futures market has remained relatively stable due to strong support from robust U.S. cotton exports in recent weeks, with the March contract closing at 81.31 cents per pound, only a 5-point decrease on Friday. Conversely, there are few adjustments made to the monthly supply and demand estimates for the 2022/23 global cotton market, with only small revisions made to production and consumption, resulting in minimal overall change.

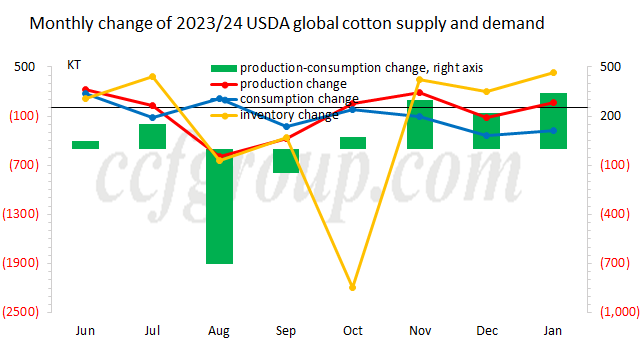

1. USDA January supply and demand change

Regarding production, USDA increases the 2023/24 production by 60,000 tons, mainly reflecting an 110,000-ton increase in Chinese production, while U.S. production is once again reduced by 80,000 tons due to a significant decrease in harvested area (however, the adjustments to U.S. cotton production are no longer surprising and have already been digested in the market, thus having limited impact). Import volumes are reduced by 20,000 tons, with USDA maintaining high expectations for Chinese imports, which are again increased by 110,000 tons to 2.5 million tons, while imports of Pakistan are decreased by 40,000 tons due to reduced demand for imports resulting from abundant domestic production. Consumption is significantly reduced by 280,000 tons, with consumption in India, Turkey, and Pakistan lowered by 70,000 tons, 20,000 tons, and 40,000 tons, respectively. Export volumes are reduced by 20,000 tons, mainly due to a slight reduction in expected Indian exports. Ultimately, ending stocks are increased by 430,000 tons, with both India and China continuing to accumulate stocks. Overall, the expectation for global ending stocks for this year has shifted from a small decrease to an accumulation. While there's a reduction of 740,000 tons in annual production, the weak outlook for consumption recovery suggests an unfavorable supply and demand situation in the global cotton market.

2. Interpretation of the USDA January supply and demand report

The adjustments made by USDA this time are not insignificant; while production is forecast higher, consumption is forecast lower. However, why has there been no significant market response to the bearish signals released? And are the adjustments made this time rational? We believe that this is because most of the adjustments in this USDA balance sheet are anticipated and have already been factored into the market, making it difficult to spark significant reactions. Today, the focus has already shifted from production to consumption, and the contraction of consumption is already an undeniable fact, leading to further declines. Although there has been an increase in production, the 740,000-ton reduction in global production for the year still provides significant support to the market bottom, and the expectation of supply constraints in 2024 remains, making it difficult for the market to experience a sharp decline. With recent improvements in U.S. cotton export data and gradual progress in downstream markets of various countries, market confidence has been boosted. However, it should be noted that this temporary rally does not necessarily indicate a turning point for the global consumption recovery in the textile and apparel market; the current weak demand situation is difficult to change, which has led to the market's consolidation around the 80-cent level in the near term.

What are the current factors influencing the cotton market? Observing the recent market fluctuations, it is clear that the industry is in a state of uncertainty, with macroeconomic sentiment becoming the dominant factor affecting the market. In addition to macroeconomic factors, what other points are worth paying attention to? Import and export data for cotton from various countries is a key indicator of their respective market influences, with China's cotton imports being particularly noteworthy. Let's look at some data: In November 2023, China imported 307,100 tons of cotton, an increase of 20,000 tons month-on-month and 73% year-on-year. In December 2023, Brazil's cotton exports reached 350,800 tons, a 100% year-on-year increase, with 220,000 tons exported to China. As of the week ending January 4, 2024, weekly export sales of U.S. upland cotton for the 2023/24 season reached 59,500 tons, a 100% increase from the previous week, with 26,700 tons to China. China has been a major player in contracting foreign cotton during the 2023/24 season, significantly affecting market fluctuations. Despite the bearish adjustments in the USDA balance sheet, it continues to provide confidence to the market. Meanwhile, the increase in Chinese purchases of yarn from Pakistan and India in the near term has also driven up the operating rate in Pakistan and India. However, the improvement this time in China is mainly due to pre-holiday stocking. As downstream textile mills finish replenishing, the cotton yarn sales will gradually slow down. It is still unknown whether the yarn inventory has flowed to the intermediate links or can be fully absorbed by the terminal. In addition, the import cotton inventory at port is also at a high level of around 480,000 tons. In the short term, it will be difficult for cotton prices to rise, and the subsequent upward movement still needs to depend on the recovery of external orders.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price