2023 spandex market review and 2024 outlook

Demand for spandex in Chinese mainland rebounded in 2023 due to the release of consumption restrictions caused by the pandemic, relatively low prices, increased downstream machinery, expansion of application and increased content. It returned to a high growth rate of around 20% compared to the previous year. However, the spandex market saw an increase in volume without a corresponding increase in price, which was particularly evident. Most spandex companies still suffered significant losses, while a few leading companies managed to gain a minor profit.

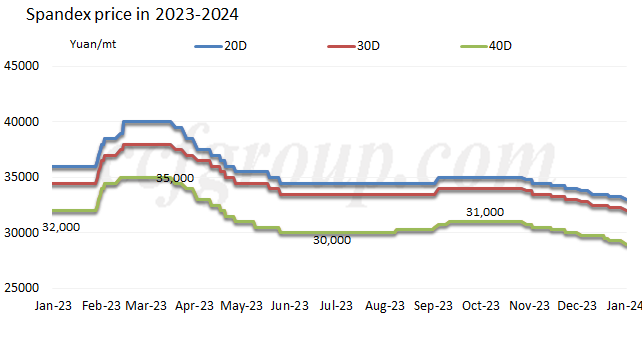

Price: M-shaped trend

Looking at the price trend of spandex in 2023, the prices curved an "M"-shaped trend. After the New Year's holiday, with the relaxation of pandemic restrictions and increased market confidence, the demand for replenishment increased, leading to a significant rebound in prices. However, by the end of the first quarter, as buying pressure eased and inventory was digested, spandex suppliers saw slower sales, resulting into downward prices. Towards the end of the third quarter, with the approaching of peak season and tight supply of PTMEG, spandex prices experienced a weak rebound. However, in late-Oct, as rigid demand turned muted and some buyers focused on digesting spandex prepared before and the upstream BDO prices fell to below 10000yuan/mt, the support from both the cost and demand sides weakened, ending up with reducing spandex prices again, and this downtrend continued until the end of the year.

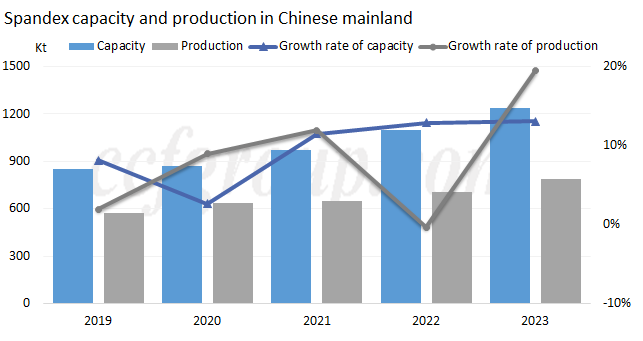

Capacity and production: up by 10-20%

By the end of 2023, the total spandex capacity in Chinese mainland reached 1.2395 million tons/year, with a net increase of 180kt/year. After deducting 45kt/year of phased-out capacity and adjusting the capacity up by 8kt/year, the net increase in capacity amounted to 143kt/year, a growth rate of 13% compared to the end of 2022. This growth rate set a new record since 2016. The spandex production in Chinese mainland approached 939kt in 2023, a YoY increase of 19.5%. The average annual growth rates of spandex capacity and production in Chinese mainland over the past five years were 9.6% and 8.2%, respectively.

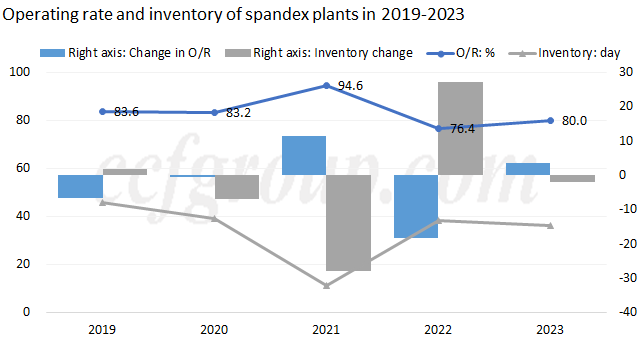

Operation: Historically second-low operation rate, slight decrease in average inventory

Based on the annual operation data of the spandex industry in 2023, the average operating rate was around 80.0%, an increase of 3.6 percentage points compared to the previous year, which was the second-lowest level since 2008. In terms of inventory, the industry saw relatively stable fluctuation with an average inventory of 36.2 days in 2023, a decrease of 2.0 days on annual basis.

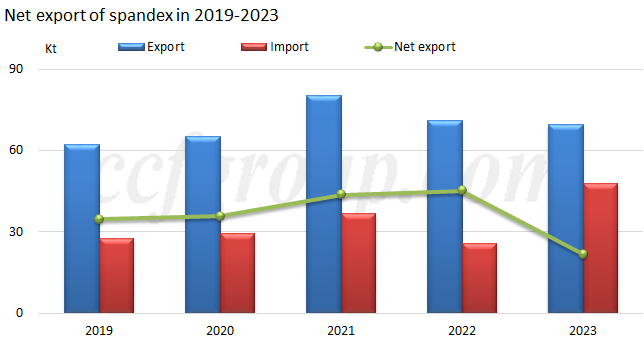

Import and Export: Sharp decline in net exports

In 2023, there was a significant divergence in the import and export quantities of spandex. Export volume decreased slightly by 2% on the year to 69,600 tons, while import volume increased significantly by 85.6% to 47,900 tons, resulting in a sharp decline of 23,500 tons in net exports, a decrease of 52% year on year. Furthermore, the average import and export prices of spandex experienced a significant decline in 2023.

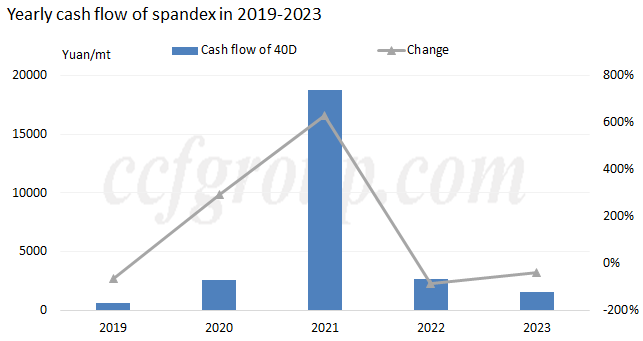

Profitability: cash flow down by around 40% year on year

The cash flow of spandex 40D was declining in 2021-2023 in Chinese mainland, with the level of 2023 close to that in 2019. The average cash flow of spandex 40D was above 17000yuan/mt in 2021, hiking on the year. It was at 2600yuan/mt in 2022, down by around 90% on annual basis. Spandex companies still faced big losses given the greatly depreciating of some inventory. The cash flow of spandex 40D apparently decreased to 1580yuan/mt in 2023, a year-on-year reduction of aroura 40%. Spandex companies were still under losses. Only some leading companies and some plants with high proportion of differential products saw minor profit.

Outlook for 2024

The spandex industry chain will still be in a peak expansion period, with an amplified growth rate in BDO-PTMEG capacity. The capacity expansion of spandex market will remain big. The spandex industry will continue to face an oversupply situation. Short-term fluctuations in the market can be expected, but in the medium and long term, prices are expected to continue to face pressure. It is anticipated that spandex prices may fluctuate around the cost line, considering factors such as industry seasonality, and there is a possibility that prices for regular specifications of spandex may reach historical lows at certain points in time.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price