Interpretation of USDA's Feb supply and demand report on cotton

Recently, the USDA released the global cotton supply and demand for February, mainly adjusting the 2023/24 production downwards again, reducing the ending stocks and overall adjustments favoring the bulls. During the Spring Festival, under the low ending stocks of U.S. cotton and with the support of good export sales, bullish funds entered the market with confidence, leading to a strong performance of ICE cotton. It broke through 90cent/lb and 95cent/lb consecutively, reaching new highs.

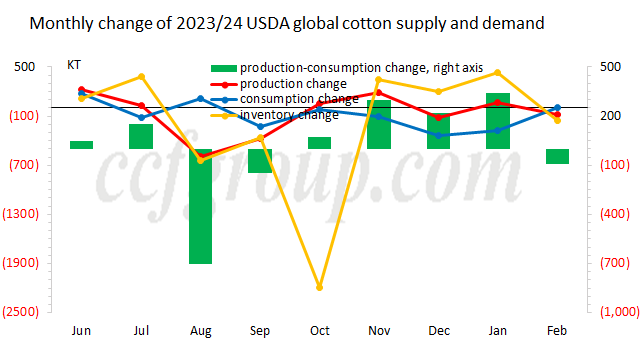

1. USDA's Feb supply and demand report

Specifically, in terms of production, USDA lowered the 2023/24 global production by 80,000 tons, mainly reflecting a reduction of 70,000 tons in Australia's production, while the much-watched U.S. production remained unchanged this time. The import volume was reduced by 40,000 tons, with USDA remaining confident in China's imports, raising it by another 110,000 tons to 2.61 million tons after an increase of 110,000 tons last month. At the same time, imports of cotton from Vietnam, which has shown strong performance recently, were raised by 20,000 tons. However, this increase was offset by reduced imports from India, Turkey, and Pakistan, resulting in a final decline in import volume. Consumption was also raised for China and Vietnam, while consumption in the U.S. and Turkey further contracted, resulting in a consumption increase of 10,000 tons. Export volume continued to be reduced by 20,000 tons, mainly due to the expected reduction in exports from Brazil. Finally, the ending stocks were lowered by 150,000 tons, with Brazil shifting from destocking to accumulating inventory, and U.S. cotton ending stocks shrinking again. Overall, global ending stocks have decreased this year. With a significant reduction in production, there are still expectations of tight supply in the future despite of weak consumption.

2. Interpretation of USDA's Feb supply and demand report

This time, the USDA adjustment was relatively small and completely opposite to the previous adjustment. Estimates for production and consumption were revised, especially the expectation of a significant accumulation of ending inventory, which did not materialize, instead releasing bullish signals, encouraging bullish funds to enter the market. The warming downstream market in China and Southeast Asian countries before and after the Spring Festival has brought confidence to the market. As finished product inventories in Europe and America gradually decrease, market expectations for future consumption have also turned optimistic. Against the backdrop of a significant global production cut this year, whether the cotton supply will maintain after demand recovers remains a speculative topic. Particularly, with U.S. cotton carry-over inventory at a low level and deliverability rates remaining low due to poor weather conditions, the market speculates that the current rise in ICE cotton may be attributed to market squeeze. However, the recovery of fundamentals is limited at present, and there may be a downward revision in the short term. In the long term, U.S. cotton may remain strong.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price