Why is spandex plant operating rate still so high

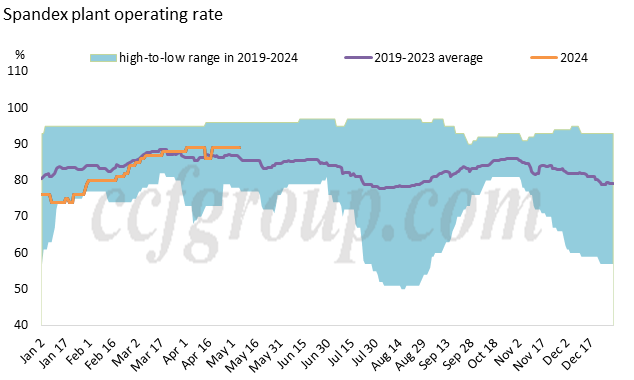

From the beginning of 2024 to the present, China spandex industry's operating rate has marginally increased to a high level (see Chart 1) and has been relatively stable. At the beginning of the year, the industry's operating rate was around 70-80%, gradually increasing before and after the Chinese New Year, reaching close to 90% during the end of March until mid-May. Why has spandex industry been able to maintain such a high operating rate?

The supply-demand situation of spandex in the first half of 2024 will be relatively better than the second half of the year. In the latter half of the year, a significant portion (around 80%) of new spandex production capacity is expected to be released. The release of new capacity in Shaoxing of Zhejiang, Ningdong of Ningxia, Chongqing, and Lianjiang of Fujian is expected to reach a total of 247,000 tons/year in the second half of 2024. However, demand growth might lag behind. The industry is burdened by an oversupply, and the cash flow pressure in spandex industry in the second half of the year may exceed that of the first half.

While the concentration in spandex industry continues to rise, there are divergent appeals among suppliers, and inventory levels vary among them. Some suppliers have high inventory levels, some around one month, some around two months or more. As of May 13, spandex industry's operating rate is slightly above 89%, with large enterprises (over 80,000 tons) operating at over 92%, small and medium-sized enterprises at around 77%. Out of the 16 spandex enterprises in China, 9 are operating at or above 90%, 4 are operating between 70% and 90%, and 3 are operating below 70%.

Leading spandex suppliers have significantly increased their production capacity last year and still have large number scheduled for this year, actively expanding their market share. The cash flow of leading companies in the industry is generally above break-even line, and a high plant operating rate helps to reduce labor and energy costs to some extent. Some spandex suppliers have vertically integrated their supply chains, facing tight capital and actively selling spandex filament to maintain normal operations. Before and after the Chinese New Year, some small and medium-sized spandex enterprises suspended operations or conducted maintenance on certain production lines for 1-2 months or longer. During plant maintenance or shutdown periods, inventory levels noticeably decreased, and although inventory levels rose slightly after plant restarts around March, overall inventory levels at small and medium-sized factories remain relatively low. As of mid-May, the average operating rate of small and medium-sized factories continues to show a slight upward trend.

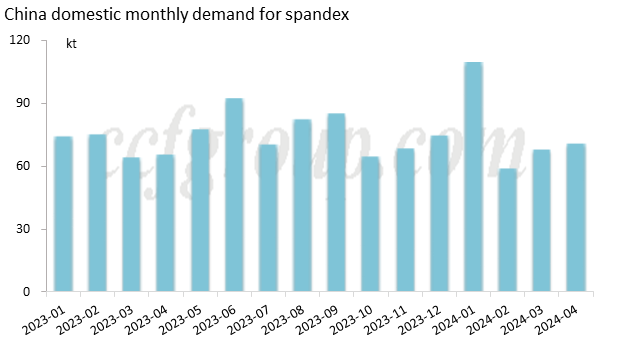

In the first four months of 2024, spandex suppliers saw a significant increase in sales, which was a major factor supporting the high plant operating rates. From January to April 2024, China domestic spandex demand increased by about 10% to approximately 310,000 tons. Trends in sun protection, sports, yoga, leisure, and other areas are still popular, and the lower spandex prices have led to a higher proportion of spandex in downstream textile and apparel products. The stable recovery of domestic sales in the textile and apparel industry and the support from textile and apparel exports also contribute to spandex demand.

BDO-PTMEG-spandex supply chain is still facing an oversupply situation throughout the year, with limited internal support in the third quarter. Attention should be paid to the impact of increased negative feedback downstream on spandex brand competition and cash flow compression on the supply side's operating rate. Subsequent focus should remain on macroeconomic factors that could bring changes to the market, such as whether the continuous increase in China domestic money supply (M2) could trigger inflation, stockpiling, and price rises, as well as the impact of supply-side reforms in the chemical industry, such as carbon emission compliance, on the effectiveness of older spandex production capacity.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price