Polyester fiber companies call for a new round of production cuts under pressure

Polyester companies successively called for production curtailment since the second quarter of 2025. Major PFY companies planned to cut production by 10% again on July 15.

The operating rate of direct-spun PFY companies and PSF plants was at 91.3% and 92.3% respectively on July 11. The run rate of DTY plants and fabric mills in Zhejiang and Jiangsu has apparently fell, staying at 62% and 58% respectively on July 11. In recent years, new DTY and fabric capacity was put into production quickly in some peripheral areas, and the products impacted the traditional production bases in Zhejiang and Jiangsu. As a result, fabric mills and DTY plants in Zhejiang and Jiangsu have run at low capacity since the beginning of year. The operating rate of polyester spun yarn plants, the downstream sector of PSF, also inched down to near 65%.

Compared with the operating rate in upstream and downstream market, the polyester fiber plants encountered apparent supplying pressure recently, especially PFY.

Sales of PFY and PSF were dull recently in factories. Downstream plants mainly purchased on a need-to-basis when the market lacked signals to move up. Factories saw big selling pressure since late-June and the inventory accumulated.

PSF companies have high sales ratio of contract goods, while PFY plants focus on spot sales. Therefore, in terms of the inventory structure PFY companies face bigger inventory burden than PSF producers. The inventory pressure is medium in history. To reserve inventory or maintain the value of inventory is the question fiber companies need to consider.

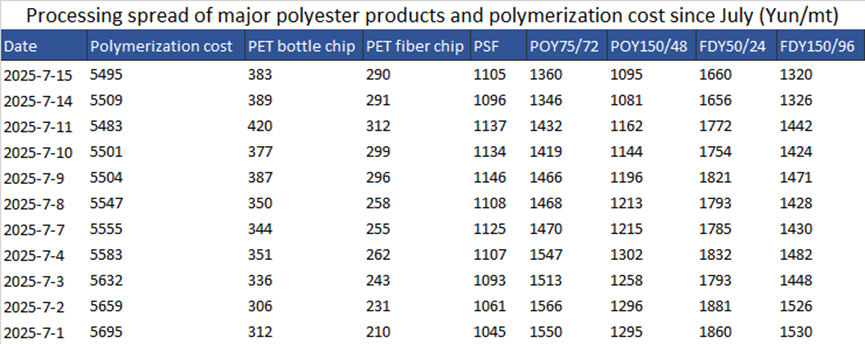

Recently, the pressure on industrial profits and losses has been concentrated on FDY, PET fiber chips, and PET bottle chips. Although the polymerization cost has continued to decline since July, among various polyester products, the processing spread of PET bottle chips, PSF, and PET fiber chips have improved compared to those in late-June. Only the price of PFY has dropped more than the polymerization cost, and their processing margins have been continuously compressed. The slight recovery in processing spread brought about by the production cuts of PET bottle chips and PET fiber chips has already shown. From the perspective of the cost line, PET bottle chip and PET fiber chip plants are still in a state of loss, while the profitability of filaments has deteriorated. The loss of FDY has intensified, with some fine denier specifications once again seeing losses expand to over 700yuan/mt, even failing to cover production costs. From this perspective, it is necessary for PFY factories to once again call for production cuts.

Recently, after the prices of various PFY products fell below the cost line, factories have slowed down their price adjustment pace. However, there is still no strong support for absolute prices, and the subsequent risks lie in the possibility of a decline in absolute crude oil prices and the compression of PXN.

In terms of operating rate of PFY companies, it is under downtrend. Some equipment with a high proportion of fine denier FDY has not been restarted after shutdown for a long time. Some factories with a high proportion of FDY and some small POY factories also carried out certain production cuts in the early stage. However, production cuts also come at a cost. Since it is still in the middle of the year, large factories that have certain expectations for demand in the fourth quarter have exercised some restraint in reducing production, which has provided certain support for the operating rate of direct-spun PFY plants. The production cuts by PSF factories are currently quite diversified, mainly focusing on sporadic production cuts of some differentiated varieties with high inventories.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price