Why PET bottle chip general trade dominance in export soars

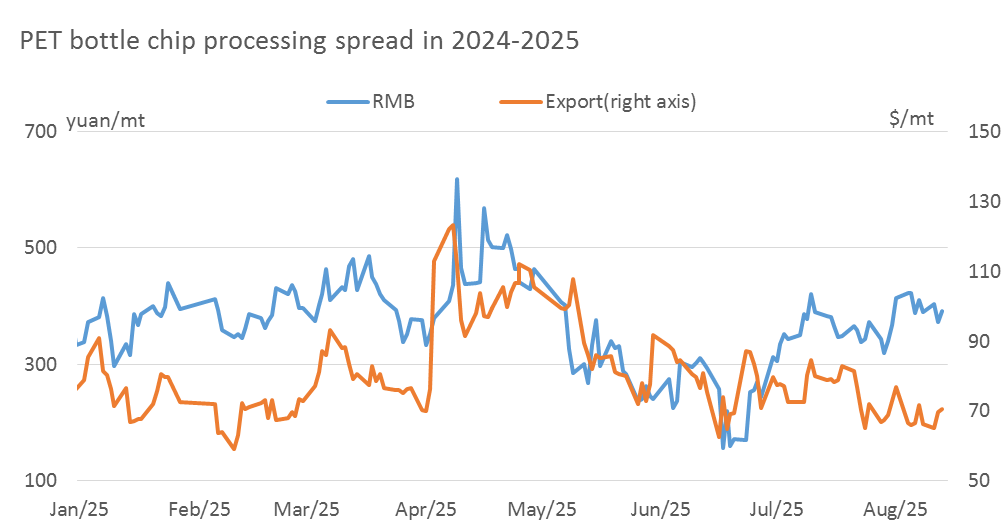

Following the concentrated production cuts and shutdowns of domestic PET bottle chip plants in July, the processing margins for both domestic and export markets temporarily improved. Downstream end-users and traders engaged in continuous restocking near the low-price levels, resulting in sustained high transaction volumes. By early August, both factory and total inventories of PET bottle chip achieved a slight decline. However, entering August, the domestic spot processing margin for PET bottle chips recovered to around 400yuan/mt, while the export processing margin was compressed again, and this compression lasted longer than in July. What exactly happened?

To state the conclusion first: The core reason for the continued compression of PET bottle chip export processing margins in August was that domestic oversupply pressure massively flowed into the export market through "domestic-to-export" arbitrage (a surge in general trade mode), leading to unprecedentedly fierce competition among export suppliers. Simultaneously, overseas demand support was relatively insufficient, allowing buyers to continuously press down prices by leveraging the intensified competition among suppliers.

The persistent activity of the "domestic-to-export" arbitrage model intensified export market competition

According to China Customs data, the proportion of general trade in PET bottle chip exports surged to nearly 30% in the first half of 2025, while trade was compressed to below 70%. This sharp increase in general trade exports (from ~2.5% in 2020 to ~29.6% in mid-2025) signifies not only a significant increase in the influence of domestic traders within the export market but also the substantive entry of the domestic sales departments of some bottle chip plants into this "RMB to USD" arbitrage game. To compete for limited export orders, traders and bottle chip plants adopted the core strategy of offering prices more competitive than the mainstream FOB offers from plants. The trader's operational logic is: purchasing bottle chip spot domestically at relatively low prices (but still above the domestic RMB net price), then exporting it at prices slightly below the mainstream plant FOB offers (but it's still above their RMB purchase cost plus operational fees and forex gains). This directly depressed the benchmark transaction price for the entire export market. It can be said that the proactive price concessions by traders and plants to secure deals are the most direct cause of the sustained compression of export processing margins.

Overseas market demand underperformed expectations, allowing overseas buyers to benefit from the situation

Although market focus shifted overseas, the actual growth in overseas demand did not meet previous optimistic expectations. Influenced by inventory digestion cycles and summer holidays in Europe and America, downstream procurement overseas slowed down periodically. Consequently, insufficient support from overseas PET bottle chip demand worsened the situation in an already fiercely competitive seller's market. When buyers are not in a hurry to restock, they have more confidence and patience to push prices down, leading to persistent downward price pressure that is difficult to alleviate quickly. This also explains why the processing margin compression lasted longer this time.

Meanwhile, to secure orders or obtain more favorable procurement costs, buyers often demanded lower CIF prices. Primarily, facing quotes from different Chinese channels (plant direct sales, traders, plant domestic arbitrage), buyers gained more room for choice and comparison, forcing Chinese sellers to accept lower transaction prices, thereby compressing export profit margins. Therefore, even after domestic PET bottle chip transaction volumes increased, plants only slightly raised RMB prices, while export offers merely maintained forward month premiums.

Expectations of domestic supply recovery in Q4 may increase export pressure

The supply reduction and inventory decline caused by the concentrated cuts and shutdowns in July formed the basis for the domestic processing margin recovery to 400yuan/mt. However, as the transition from Q3 to Q4 approaches, some plants (e.g., Wankai, Yisheng Hainan) are expected to gradually resume production or increase operating rates. Domestic supply volume is anticipated to rise. While summer factors like substantial discount coupons from food delivery platforms boosted beverage consumption and thus temporarily increased end-use packaging demand, the overall domestic demand remains fundamentally tepid. Furthermore, new capacity from Fuhai is still slated to enter the market later. Currently, it seems the new supply cannot be fully absorbed domestically, inevitably leading more material to seek export channels. This expectation will further intensify supply pressure in the export market, strengthening the bargaining power of overseas buyers.

In summary, this phenomenon of "internal competition spilling over externally," while increasing export volumes via general trade in the short term, comes at the cost of sacrificing the entire industry's export profits (processing margins). It marks a transition for China's PET bottle chip industry from the relatively stable plant direct sales model of the past to a more complex, fiercely competitive, and lower-margin multi-channel battle mode. The healthy development of the industry urgently requires addressing structural overcapacity and establishing a more rational market order.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price