Development of China's PET bottle chip industry

PET bottle-grade chips are the core packaging raw material used to manufacture transparent containers such as beverage bottles, edible oil bottles, and personal care packaging. In China, the development of this industry is nothing short of an epic saga of industrial upgrading - evolving from ground zero, overcoming technological barriers, expanding in scale, and eventually becoming a global leader.

According to data from CCFGroup, after years of development, China's total capacity for PET bottle-grade chips has reached 21.68 million tons, accounting for roughly half of the global capacity (with global PET chip capacity at 42.62 million tons in 2024). In terms of exports, China's export market share has reached approximately 57% in 2024, making it the world's most important production base for packaging-grade PET chips.

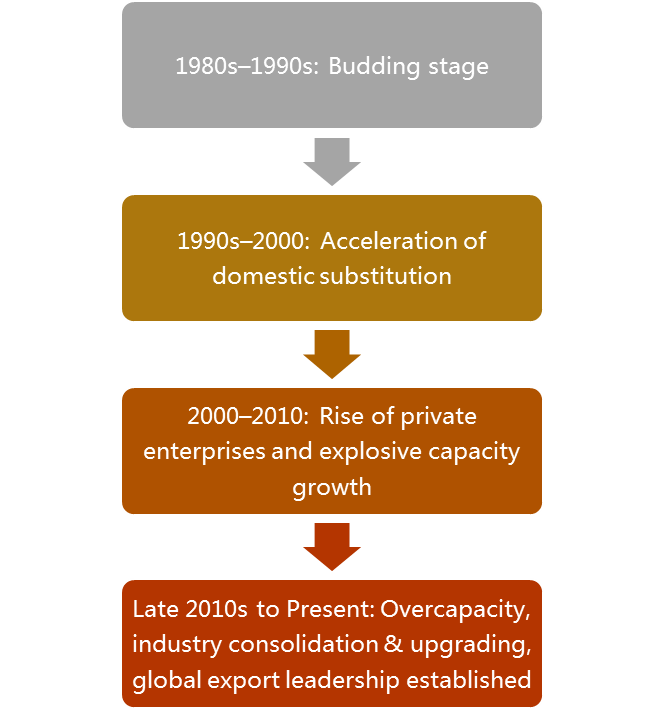

1980s–Early 1990s: Blank Slate and Exploration Phase

During the early days of China's reform and opening-up, the domestic beverage and edible oil industries began to emerge, generating demand for PET bottle-grade chips. However, at that time, China had no production capacity at all - all PET chips had to be imported at high prices, severely constraining downstream development and consuming large amounts of foreign exchange. To break through this bottleneck, the government supported enterprises in introducing foreign technology and equipment. Nevertheless, due to limited technological absorption capacity, lack of supporting raw materials (e.g., PTA, MEG), unstable product quality, and high costs, the industry developed slowly, with small-scale capacity and continued heavy dependence on imports.

Mid-1990s–2000: Technology Breakthrough and Initial Scaling

Led by state-owned enterprises such as Yizheng Chemical Fibre, China began to digest, absorb, and innovate upon the initially imported technologies and equipment. Domestic engineers worked diligently to master key process technologies such as continuous polymerization and solid-state polycondensation (SSP). As localization of equipment gradually improved, both investment and production costs dropped significantly.

With technology maturing and demand surging - particularly in the carbonated beverage and bottled water segments - a number of localized production units were built and put into operation. By around 2000, China's PET chip capacity exceeded 500,000 tons/year, forming an initial industry scale. Localization rates rose significantly, reliance on imports began to decline, and domestic demand was increasingly being met.

2000–Mid-2010s: Rise of Private Enterprises and Full Industry Chain Integration

The 2000s witnessed the rise of private sector players and the steady development of China's polyester value chain (PTA and MEG), laying a solid foundation for China's future global leadership in PET chips. A large number of private enterprises - including Sanfame Group, China Resources (formerly Hualei), Yisheng Hainan, Yisheng Dalian, Chongqing Wankai, and Zhejiang Wankai - seized market opportunities.

With their flexible mechanisms, efficient decision-making, and continuous capital investment, they entered the PET chip sector on a large scale and became the main drivers of industry expansion. Fueled by robust domestic demand (spanning beverages, cooking oil, personal care, and PET sheet applications) and relatively low technical barriers compared to upstream PTA, China's PET chip capacity grew explosively. Projects were launched across the country, and single-line capacities expanded from a few tens of thousands of tons to hundreds of thousands of tons.

Late 2010s to Present: Overcapacity and Industry Consolidation

After years of rapid growth, the PET chip industry is now facing periodic overcapacity and intensified market competition. The industry has entered a phase of deep consolidation, with leading players leveraging advantages in scale, cost, technology, and customer relationships to gain greater market share. Through mergers, acquisitions, and elimination of outdated capacity, industry concentration has risen sharply. Key players - such as the Yisheng Group, Wankai Group, Sanfame, and China Resources - now account for nearly 80% of total capacity.

Since the 2000s, the Chinese PET bottle chip industry has undergone several major capacity expansion waves, notably in: 2001–2002, 2004–2005, 2009–2010, 2012, 2017–2018, 2023–2024. During these periods, average annual capacity growth ranged from 20–30%, with some individual years exceeding 100%.

Looking at the past 30 years, among currently operating plants:

Units over 20 years old account for 1.65 million tons, accounting for 7.6% of total capacity. Most of these have been upgraded or can be repurposed for other chip products.

Units aged 10–20 years account for 4.96 million tons, or 23%.

Nearly 70% of total capacity was added in the past 10 years, with over 8.4 million tons of new capacity from Yisheng and Sanfame alone between 2016 and 2025 - accounting for 56% of capacity additions during that time.

Generally speaking, due to the cost-sensitive nature of PET bottle chip production, years of high raw material price volatility tend to result in the elimination of older, less competitive units, such as those owned by Nan Ya Kunshan, SK Zhenbang, and Hainan Shengzhiye.

From a scale perspective, 64% of China's PET chip production lines have single-unit capacities of 500,000 tons or more, with over 90% of these built in the last 10 years. Plants with total capacity over 3 million tons now account for 79.3% of the industry, highlighting significant economies of scale and high industry concentration.

In just over 30 years, China's PET bottle chip industry has transformed from being entirely import-dependent to self-sufficient and now leads the world in capacity, technology, and exports. However, rapid development has also brought growing pains, particularly supply-demand imbalances. Nevertheless, it is expected that the industry will gradually transition toward a new phase of high-quality development.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price